電動車專題|電動車需求衰退下車用科技發展核心(中)

作者:智璞產業趨勢研究所綠能中心主任 余適伯

Automotive upgrading must continue, the short-term automotive industry chain enterprises to profit lock three core

Although the demand for electric vehicles has slowed down, the overall automotive market still maintains an annual sales volume of more than 80 million units, with a growth rate of 2~4%. In order to continue to maintain the market share of its own brand of vehicles to face competition from Chinese car manufacturers, the upgrade of automotive technology will continue to be an important key to gain the attention of consumers in the future, and the profits of enterprises in the automotive industry chain will be based on the automotive industry. The profitability of enterprises in the automotive industry chain will be based on the three core areas of automotive technology upgrading.

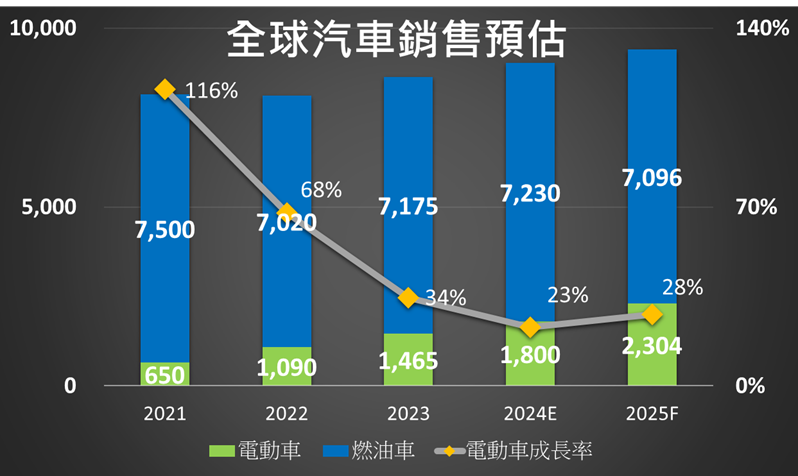

Electric cars are not the only thingThe growth rate of electric vehicle sales in the past three years (Figure 3) shows that although sales are still on the rise in 2024, with an estimated growth rate of 23%, the trend has slowed down compared to the past three years when sales were 1,19%, 68%, and 34%. Under this trend, fuel vehicles will still be the mainstream of automobile sales in the next three years, and the golden crossover between electric vehicles and fuel vehicles has not yet arrived in advance. From this, we can also see that if automobile-related enterprises take electric vehicles as the only sales target of their products, the base of profits will not be enough to push up revenue growth, so automobile-related enterprises should target on products that can be provided to both electric vehicles and fuel vehicles, and use "electric vehicles are not the only ones" as the basis for growth. Therefore, automotive-related companies should focus on providing automotive products for both electric vehicles and fuel vehicles, and use "electric vehicles are not the only thing" as the first core of short-term performance growth.

Chart 3 Estimated Sales of Electric Vehicles

Source: Ward Intelligence; Collated by Wisdom Industrial Trend Research Institute 2024/03

Production cost orientation:In this wave of price cuts, the cost problems of various car makers have been magnified and examined. Among the many non-Chinese car makers, except for Tesla, almost no car maker has been able to make price cuts to grab the market on the premise of maintaining profitability. But even for Tesla, in this one-year price cut period, the speed of cost optimization could not keep up with the magnitude of its own price cuts, and suffered a sharp decline in gross profit margin. On the other hand, due to the subsidies provided by the Chinese government for EVs in the past few years and the preferential treatment for related industries, China's EV industry has become more mature than overseas in terms of production capacity, related raw materials, and infrastructure, which has led to a higher self-manufacturing rate of parts for China's EV factories, with the best example being the leading EV seller, BYD. The best example of this is the current EV sales leader "BYD", whose EV model "Seagull" has a parts production rate as high as 75% in UBS's disassembly report, which illustrates the brand's amazing car-making ability. In the face of price cuts to grab market share, the ability to control costs with a high parts production rate has allowed Chinese car makers to demonstrate a quick response advantage in price wars. On the other hand, European and American automakers have inherited the model of the past fuel-car era, relying on outside vendors as parts suppliers. The advantage of this model is that it spreads out the risks in the supply chain and avoids the collective collapse of the entire industry chain when the market environment is not favorable. However, in a price war, the speed of cost optimization is relatively slow, which also puts European and American carmakers in a passive situation this year. Therefore, in the future automotive upgrades, the pursuit of "cost orientation" based on the premise of gross profit improvement will become the second important core of vehicle manufacturing and vehicle design for European and American automakers. In addition, in the past few years, in response to the demand for rapid vehicle manufacturing in the era of electric vehicles, more Tier 2 and Tier 3 suppliers have had the opportunity to engage in dialogue with vehicle manufacturers to participate in the design of new vehicle models. It is expected that in the pursuit of the core demand for cost in the future, suppliers that possess the integration capabilities to achieve rapid design, efficient production, and module shipment will become an important partner for brand manufacturers.

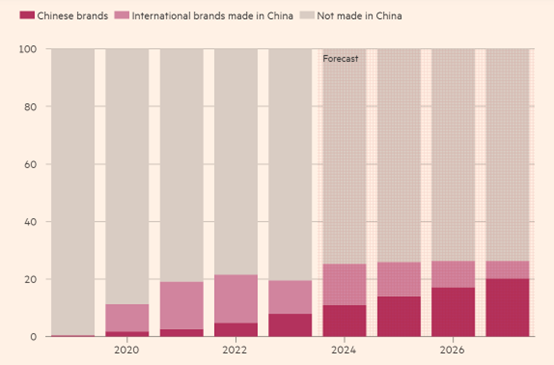

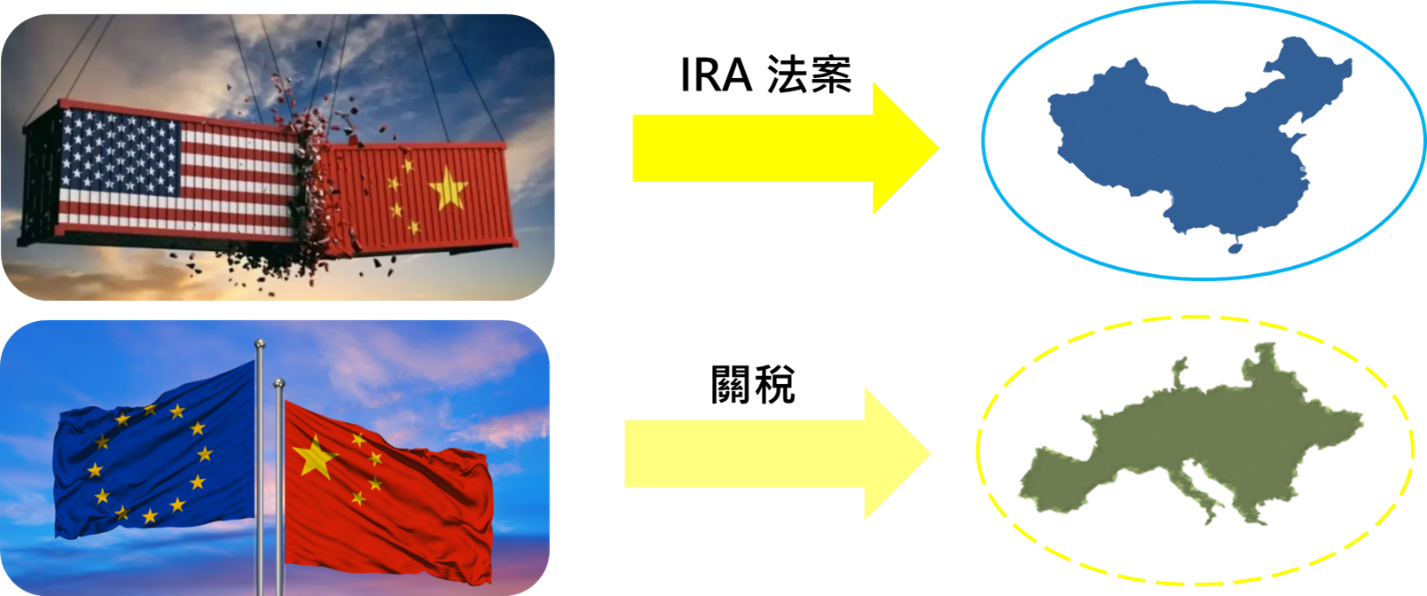

Geopolitical factors:The trade war between China and the United States, which started in 2016, extends from the technology sector to the electric vehicle sector in 2022. In order to prevent Chinese automobile manufacturing capacity from controlling the electric vehicle market, the U.S. government will introduce the "Inflation Reduction Act" (IRA) at the end of 2022, which introduces a $7,500 subsidy for new vehicles in the electric vehicle sector, as well as tax breaks for electric vehicles, and the conditions of the subsidy are mostly based on the appeal of the United States manufacturing. The subsidy conditions are mostly based on U.S. manufacturing, requiring key raw materials to come from countries with which the U.S. has signed free trade agreements, and restricting the entire vehicle and key components (such as battery systems) to be assembled in the U.S. in order to qualify for the subsidy. After the implementation of this law, the U.S. EV market is now independent of Chinese EV brands, and has become a net for European and U.S. brands as well as U.S.-based EV start-ups, with Tesla becoming the biggest winner in the market, with more than 50% of its revenue coming from the U.S. in the past few years. In February 2024, to further expand the Made in China conversation from EVs to the automotive industry as a whole, U.S. Senators have proposed a 1,25% tariff on cars made in China to prevent China from causing unsustainable damage to the U.S. auto industry with its low-cost cars. If the bill is passed, it will certainly have a significant impact on the industry as a whole. The previous model of manufacturing parts in China and supplying them to assembly plants in China will no longer be applicable to the U.S. market. Considering the logistics costs and the possibility of further adjustments to the bill, "invested in the U.S." and "made in the U.S." will be the trend for automotive suppliers. On the other hand, the European market on the other side of the ocean has maintained a relatively open attitude toward products produced in China, which has led to the European market becoming one of the main targets for Chinese automakers to shift their strategies abroad. According to the Transport & Environment report (Figure 4), section to the end of 2023 European electric vehicle market share of Chinese-produced electric vehicles is 18%, if the progress in 2024 will exceed 25%, which makes the European Union feel uneasy is that in the past, most of the cars sold in Europe are made in China with European brands, and the trend has been slowly changing. This trend has been slowly changing in the first half of 2023, the Chinese brand of electric vehicles, has reached 8% market share, this figure is expected to exceed 20% in 2027, by then made in China and sold to Europe's electric vehicles, will be mostly China's own products.

Chart 4 Proportion of EVs from China in the European market

Source: Transport & Environment

At Auto Munich 2023, we can already see that Chinese brands including SAIC MG, BYD, Geely, Xiaopeng and RISO have all proposed to consider Europe as the next key sales region for their brands. In view of this, the European Union proposed in November 2023 that it will target electric brands from China and investigate whether the use of welfare policies such as tariff exemptions, land concessions, and subsidies for the construction of factories has resulted in an unfair competitive advantage with local car manufacturers, and will use this as a basis for levying tariffs. In conclusion, with both the U.S. and the EU rumored to levy tariffs on vehicles from China, it is speculated that "geopolitical factors" will be the third core of the automotive industry in the future (Figure 5), and that enterprises or industrial chains that can make advance layouts in response to regional production requirements will be direct beneficiaries of the next wave of technological upgrades in the automotive industry.

Figure 5 Geopolitical Protectionism in the Automotive Industry

Source: Ji-Pu Industrial Trend Research Institute 2024/03