關稅戰專題|川普半導體關稅解析之美中半導體相互依存關係

Author: Mr. Lin Weizhi, Executive Vice President, Ji-Pu Industrial Trend Research Institute

As the Trump administration further escalates the intensity of the tariff war against China, the policy contours for China's semiconductor and critical technology equipment are becoming clearer. The overall policy direction has been to put pressure on China's technology development through export controls, national security investigations and negotiation mechanisms. Continuing the analysis from the previous article (Analyzing the Motivation and Risks of Trump's New Tariff Policy), from the overall logic, additional basic tariffs (10% base rate or 20% fentanyl tariff, etc.) should be the current situation, but high tariffs are not the ultimate goal, but a negotiating tool for the Trump administration to achieve the following strategic goals: first, to continue to slow down China's technological rise; second, to

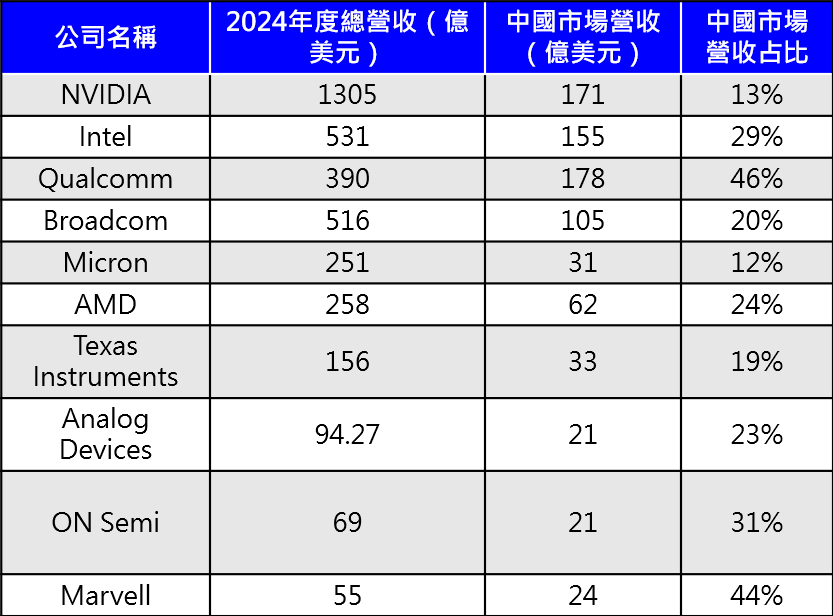

Although some electronic products (e.g. smartphones, laptops, semiconductors) are not on Trump's list of 301 pain points for the time being, Secretary of Commerce Howard Lutnick has already said that these exemptions are only temporary and that they may still face new tariffs in the future. Semiconductor tariffs may be one of the tools that the U.S. wants to use, but when you look at it, is it Chinese semiconductor companies that need the U.S. market more, or is it U.S. semiconductor companies that need the Chinese market more? First of all, in the advanced process, 10 nm technology node, China only SMIC can produce 7 nm wafers, and due to capacity constraints in addition to Huawei cell phones have not been heard of significant external order manufacturing, so the part of China's advanced process will not be discussed for the time being. In the mature process segment (≥16 nm), according to TrendForce, if we combine the capacity of China's local foundries (e.g., SMIC, Huahong, JHI, etc.) and foreign companies with fabs in China (e.g., TSMC's Nanjing fab, UMC's Suzhou fab), as well as China's integrated device manufacturers (IDMs) (e.g., CR Micro, Silan Micro, SMiT, etc.), by 2024, China will have the largest share in the world's mature process segment (≥16 nm). In 2024, China's share of global mature process wafer production capacity will be about 34%, while TechInsights data shows that China's overall IC self-sufficiency rate in 2024 will be about 30% (including memory), which includes 10%~12% of self-manufacturing by China's enterprises and 18%~20% of contribution by foreign enterprises, which is the highest in the world. These include 10%~12% produced by Chinese enterprises and 18%~20% contributed by foreign-invested enterprises, such as Intel, TSMC, Samsung, SK Hynix and other foreign-invested enterprises in China. This data shows that Chinese ICs are unable to cope with their own market in China, let alone export. On the contrary, the top 10 U.S. IC companies (including IDM and Fabless), in addition to the ICs shipped to China for assembly needs, each company will have about 13%~46% of revenue in 2024 from Chinese OEMs, as shown in Table 1 below.

Table I. Top 10 U.S. IC Companies' Total Revenue and China Revenue Share in 2024

Source. Financial reports; Organized by Ji-Pu Industrial Trend Research Institute.

Among them, U.S. companies Marvell (44%), Qualcomm (46%) and Intel (33%) have long relied on China's mobile phone/data center OEMs, and their operational resilience will be the most tested in the second half of the year if U.S. export control is tightened again; Power Analog and MCU suppliers such as TI and ADI, Power Analog and MCU suppliers such as TI, ADI, Microchip mainly serve the industrial/automotive market, and the recovery of China's electric vehicles and industrial control chain may become the growth highlights in 2025, but the price pressure will rise at the same time. Meanwhile, China also announced on 4/11 that it has strengthened the tax system on wafer flow at the wafer's place of origin. China has levied 25% retaliatory tariffs on some U.S. semiconductor products since 2018, but since there is no mandatory flow restriction, in the past, if a wafer vendor said "this wafer is sealed and tested in Malaysia", China would sometimes not be able to find out the place where the wafer was flowed and would just let it go. However, the new system strengthens loophole prevention and requires the submission of PO or process documentation to support the customs declaration. In other words, China no longer allows you to "obfuscate the place of origin" by referring to the place of design, branding, or testing. This could have significant business implications for many U.S. chip companies.At present, it seems that if the United States, China and each other based on the origin of the chip to take additional tariffs, the impact on the U.S. is relatively large, if the final Trump targeting the terminal product significantly levied semiconductor origin of the relevant tariffs, I think its purpose is not to target China's semiconductors, but rather against Taiwan, South Korea, Japan, and other Asian chip production chain.

According to Omdia's research, China's annual local sales account for about 38% of ICs, and 48-50% of ICs used in re-exported end-user products, which means that China's IC consumption accounts for half of the global IC sales every year, which is a huge amount of more than $300 billion. In addition, China's proactive efforts in research and semiconductors, such as DeepSeek R1 released by DeepSeek at the beginning of the year, which utilizes a small amount of resources to provide a cost-effective AI open-source business model; the use of repeated exposures to continue to break through the limits of advanced processes without EUV exposure machines; and the continued increase in the purchase of semiconductor equipment regardless of the market situation, expanding the production capacity of mature manufacturing processes. I believe that the Trump administration would like to proactively deal with China's influence here, not only to block China's development, but also to be accountable to its domestic supporters. Therefore, summarizing the above assumptions and inferences, I believe that the U.S. semiconductor measures against China will strengthen the current loopholes and continue to tighten the restrictions as follows:

- Expanded control of AI chips:Also based on the standard of computing power/bandwidth/power consumption (computing power density, FLOPS/W x Die Area), the current lower limit is revised downward to cover a wide range of inference chips in addition to training chips. Currently, it mainly restricts GPGPU-related chips such as Phaidon and Supermicro, but in the future, it is likely to include end-use (inference applications) in the scope of the new export audit.

- Expansion of TSMC's OEM limitations for Chinese or Chinese-invested customers:Currently, companies on the Entity List, such as Huawei (Hesse Semiconductor) and Calculator Technology, are prohibited from placing orders at TSMC, and we do not rule out the possibility of expanding the list of restrictions in the future to limit the number of relevant Chinese companies. In the future, we do not rule out expanding the restriction list to restrict the relevant Chinese companies. We may strengthen both the "Entity List" and the "Process Node (China: Technology) Level Restrictions", and in the most stringent case, we do not rule out entering into a comprehensive review and authorization mechanism. Expanding the limitations of process nodes, the current comprehensive control of products after FinFET and the following, the future may be expanded to part of the product (company) is prohibited in the TSMC Nanjing plant production, and even to 28 nm to do the limitations (there may be a relative degree of difficulty, therefore, if you want to limit the possibility of part of the product); packaging part of the original 16 nm and the following wafer if the final packaging is not in the BIS If the final packaging of 16nm and below wafers is not completed within the BIS "approved OSAT" white list (Supplement No. 7 to Part 740), TSMC will refuse to ship the wafers. White List members are located in non-China/Macau regions (e.g. ASE, Amkor, PTI, SPIL, Fabrinet, Giga Solution, etc.) and may be extended to include some 28nm products.

- Expansion of semiconductor process equipment, EDA and IP export ban:About Semiconductor Equipment(math.) genusI don't believe that the US will have the courage to ban the import of all mature (12") US-made equipment into China in one fell swoop, but it may do further control on advanced packaging equipment (U.S.-China Technology War Driving the Semiconductor IndustryThe U.S. may strengthen software license audits based on this expanded EDA ban; in terms of IP, x86 and ARM IP licenses may also be included as part of the blocking strategy. The U.S. may expand the scope of prohibited versions of EDA and strengthen software licensing audits; in terms of IP, the IP licenses of x86 and ARM may also be included as one of the blocking strategies. x86 is the original architecture of U.S.-based company Intel, and it is relatively easy to restrict it, but the popularity of the application side of the Chinese enterprises may be more of a declarative than a practical significance; and for ARM, if it is really banned, it will be more difficult for Chinese designers to get rid of it. If ARM is really banned, the Chinese design industry will be relatively sensitive. However, ARM is a company registered in the United Kingdom, subject to the United Kingdom and the European Union regulations, not directly subject to U.S. export control constraints. If you want to restrict, the United States may need to use more than 25% more than the use of U.S. development tools (EDA) or software modules, through the EAR rules require U.S. permission and other related regulations to do indirect requirements; or the U.S. side can advocate FDPR rules and military end-use, the direct definition of the relevant China will need to authorize the enterprise (such as Huawei, Cambridge, BYD Semiconductor, etc.) for military security purposes, so that the British government and the United States can coordinate. This would allow the UK government to coordinate with the US to restrict ARM (China) by making specific Chinese companies unlicensable (military use blocking). However, if this action is banned, the first one to object will be ARM itself, because this action will accelerate the development of open source architectures (e.g. RISC-V + open source) and suppress ARM China's status, and it will be very difficult for the U.S. to really adopt this restriction, but no one can say for sure with the current level of insanity in the game between the two countries.

- Tariffs on ICs for end productsAccording to the analysis in the first half of this paragraph, if the U.S. imposes an overall and substantial semiconductor origin tariff, Taiwan, Korea, and Japan will be the ones who will be relatively frustrated, not China. However, in terms of the current interaction between the U.S. and China, the U.S. has continued to raise the tariff threshold, creating a high-pressure negotiation situation (possibly from 54%->125%->145%->245%) to determine that it is not justified not to impose additional tariffs on semiconductors. Therefore, I think the possible direction of the levy will be.Increase the percentage of U.S. value (currently requiring at least 20% under Section 01.34), impose additional tariffs on "some" end products that use chips manufactured in China or sold by Chinese companies, and impose a time limit for replacementsThe production includes IC manufacturing and packaging testing. For brand owners, most of the big chips, such as CPUs and GPUs, are produced by U.S.-based companies or by companies such as TSMC and Samsung, which have already announced their intention to invest in the U.S. Because of the temporary compliance with the U.S. value and the short-term requirement to switch their production capacity to other production sites, it is almost impossible. However, it is relatively easy to replace some of the mature chips that Chinese companies can produce, such as MCUs, Power Analog, CIS, DDIC, etc., with U.S. or non-Chinese companies. In the past, due to the relatively low price of these products and the time required for reliability verification, manufacturers were reluctant to replace them even if there were good alternatives in the market.

Finally, the U.S. strategy towards Chinese semiconductors has evolved from "one-size-fits-all tariffs" in 2018-2020 to a "one-size-fits-all tariffs" strategy that may evolve into a "one-size-fits-all tariff" strategy.Technological locks + Nominalized tariffs". The U.S. says it needs to minimize its trade deficit, but it is likely to sharply restrict China's chip purchases? This may seem like a contradiction, but in essence the goal is to reorganize its supply chain and shift its core as much as possible. In the short term, this could tighten the Biden administration's export controls first and tariffs second.Austerity followed by taxation"In the medium term, if the Section 232 investigation finds that the tariff on 25-35 % chips is a "threat to national security", the tariff will become the main force to press China (and also affect the supply chains of Taiwan, Korea, and Japan). However, the "two-way asymmetry" between U.S. chip companies' high dependence on China's revenue and China's even deeper dependence on U.S. equipment/EDA has not yet been fundamentally altered, and the U.S.'s excessive escalation of pressure will inevitably jeopardize its own industry and inflation control, while giving China the impetus to accelerate the expansion of its mature processes and breakthroughs in open-source RISC-V architectures.In the second half of 2025, the U.S. and China are expected to tug-of-war over the "depth of technology blockade" and the "scope of tariffs/taxes," while the global semiconductor supply chain is expected to hedge against policy uncertainty with regionalized, multi-site backup.As for Taiwan enterprises, according to the current observation, those who have the ability to invest overseas should be able to get out of the turbulence and stabilize, but those who do not have the ability to do so will have a relatively hard time or even face a battle for survival and need government assistance. However, the U.S. itself is also deeply affected by the asymmetry of the Chinese market and the dependence on assembly capacity, such as Qualcomm, Marvell, Intel's China revenue accounted for as high as 30% to nearly 50%; Apple, Dell and other system factories are even more difficult to fully disengage in the short term, so any extreme tariffs or export bans are with the risk of extinction.The future policy is most likely to be a tug-of-war of "phased pressure + negotiation for bargaining chips" rather than a one-time total blockade. For the supply chains of Taiwan, Korea, and Japan, the biggest challenge will be how to maintain node flexibility and technological leadership between geopolitics and market demand.