Seminar|Key Technology Trends in 2023 (Top)

Looking back at the global technology and semiconductor environment in 2022, from the beginning of the year 2021, the expected more material, repeated orders, automotive industry shortage of wafers and production stoppages, to the inflation more than the Federal Reserve has continued to raise interest rates to curb, and then to the market growth correction, to go to the inventory, and other negative issues surfaced and so on, the global monopoly covered by a piece of stagnation or even recession in the heart of the worry. The entire 2022 market seems to be like a three-warmer, oscillating up and down. In addition to the escalation of the U.S.-China technology war, the U.S. technology blockade of mainland China has further impacted the semiconductor industry, and compared to the previous ban, the scope of "advanced manufacturing processes" has been expanded, which has begun to affect the performance of the relevant companies. 2023 is bound to add more uncertainty and turbulence to the global technology and semiconductor industries, but under the observation of the general trend of changes in the market, we can still see that some industries or products that can continue to grow in 2023, like However, under the observation of the changing market trends, we can still see some industries or products that can continue to grow in 2023, such as the automotive industry, automotive electronics and semiconductors, HPC and server LEO. The Chipotle Industry Trend Research Institute has summarized the three major technology trends for 2023 based on the direction of the general environment, as well as industry observations and analyses.

2023年重要科技趨勢 I

自駕車,我們認為在2023年將會持續成為一個很熱門的議題。2016年賓士母公司戴姆勒集團在法國巴黎車展上,發表了一個以「人」的需求與渴望為出發點的「C.A.S.E.」品牌未來核心策略理念,整合了C:Connected車聯網科技、A:Autonomous自駕技術、S:Services & Shared共享與服務與E:Electric電能驅動共四大面向,為未來的移動世界規劃一個願景和藍圖。此後,全球汽車產業的發展持續往這四個方向邁進。到不是賓士集團的影響力大到全世界都跟著他們走,而是他們領先判斷出未來乘用車以人類需求出發的四大趨勢。換句話說,在CASE 趨勢風潮下,整車設計被驅動朝著電動化、電子化、智慧化的機能前進。在汽車智慧化當中自動駕駛與智慧座艙將是兩個主要發展軸線,各大車廠也持續在這兩個主軸上佈局。其中市場上佈局在自動駕駛領域上的持續朝兩大方向分別是:看得更清楚、想得更仔細更全面來努力。

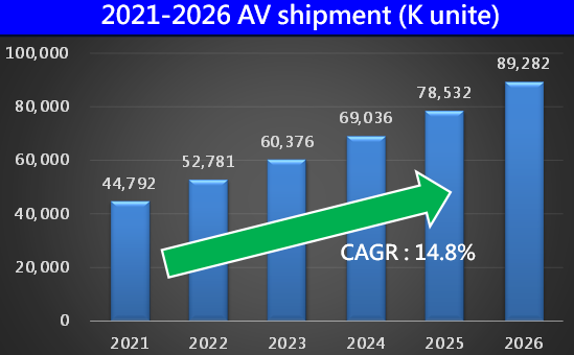

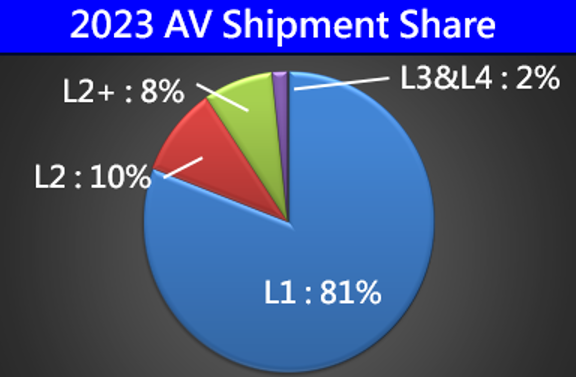

在疫情全球大流行期間,全球汽車市場遭受到新車銷售需求下降、供應鏈中斷和晶片短缺等挑戰的困擾,然而,隨著全球市場恢復到疫情前的增長階段,對新車的需求正在復甦。車廠修正了他們的自駕車的發展策略、重新確定投資的優先順序,並將重點轉向引入具有部分和半自動駕駛技術的新車。歸納一下近半年市場上的消息。Mobileye 一直在積極開發硬件技術和軟件解決方案以促進消費者和商業應用中的自動駕駛。今年的客戶群包括福斯、吉利、BMW、福特和本田等大品牌在消費者的應用,以及 Transdev、SIXT 等公司在自駕計程車中的應用。目前已在美國IPO;NVIDIA 與M-Benz在旗下所有自駕車相關要求方面的首選合作夥伴,從計算硬件、人工智能 (AI) 建模、仿真、測試和驗證;Qualcomm 與GM汽車合作,為數字駕駛艙、下一代遠程信息處理系統和未來的高級駕駛輔助系統提供動力,以滿足不斷變化的需求,為消費者提供一流的體驗;DENSO 和豐田正在合作研究和先進車載半導體的開發,以利用豐田在移動性方面的知識加快開發速度;Bosch與M-Benz合作開發和部署高度自動化的無人駕駛(SAE 4 級)車輛;GM先進的駕駛輔助技術,包括 Super Cruise、Ultra Cruise 和 Cruise Origin,自駕計程車有望在 2023 年實現商業化。到 2023 年,Super Cruise 將在通用汽車全球品牌的 22 款車型上提供等等。從上面新聞不難發現,以往在封閉的汽車產業鏈當中,IC設計公司屬於Tier3甚至Tier4,鮮有與Tier1的直接合作。然而在近年來的風潮下,這半年看到許多IC設計公司與Tier1或車廠合作開發自動駕駛相關晶片。從另一個角度來看,其實代表著車廠及IC設計公司都看好自駕車趨勢。圖1是市調機構2022年公布2021~2026年自駕車依據自駕等級的出貨數量。2023年預計自駕車出貨超過6千萬台,其中L1 占81%居首、L2占10%、L2+占8%、L3+L4占2%。L2首次突破10%占比,L2+接近8%。

圖1-1. 2021~2026年自駕車出貨台數

資料來源 : IDC; 智璞產業趨勢研究所整理 2022/10

圖1-2. 2023年自駕車等級出貨占比

資料來源 : IDC; 智璞產業趨勢研究所整理 2022/10

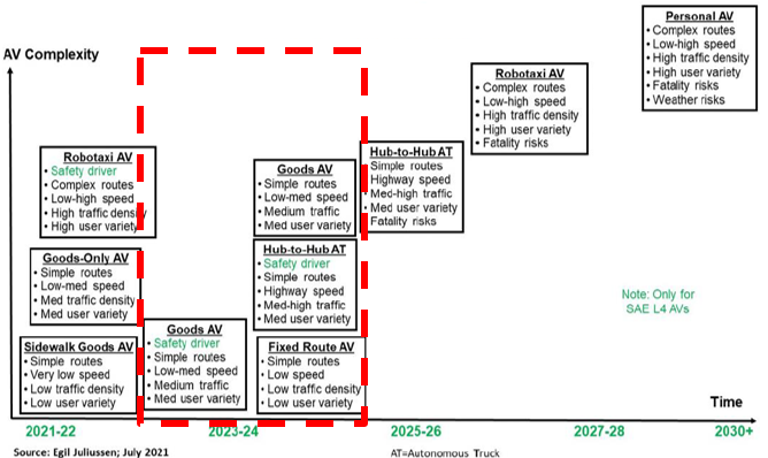

而2023年,我們最有機會看到的先進自駕商業化會是物流車、計程車與卡車在簡單路線的商業自駕,也就是>L2的自駕車商轉,如圖2。

圖2.自駕車使用範例進化預測

資料來源 : EgiI Juliussen, 2021

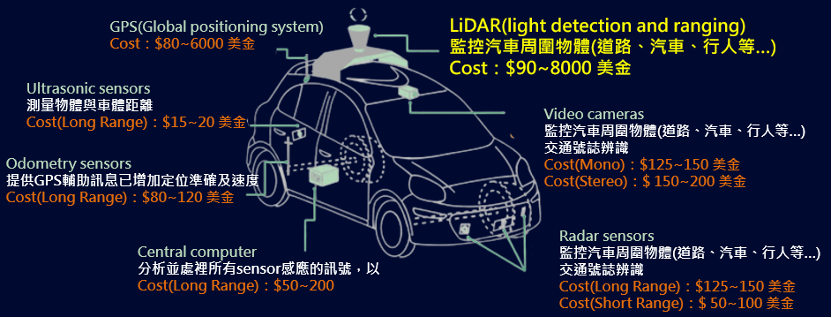

雖然台灣的汽車製造工藝不是特別的出色,但在汽車零組件上面,是有在國際上表現不錯的廠商。根據美國能源部過去發布的資料,若從一台自駕車上的硬體成本出發,GPS約 $80~$6000, Lidar監控汽車周圍物體約$90~$8000, Ultrasonic sensors測量物體與車體距離約$15~$20, Odometry sensors提供GPS輔助訊息已增加定位準確及速度約$80~$120, Video cameras & Radar sensors監控汽車周圍物體(道路、汽車、行人等…)交通號誌辨識約$125~$200(Mono/ Stereo), Central computer分析並處裡所有sensor感應的訊號約$50~$200。其中我們看好成本高居整台車之首的Lidar系統。

圖3 自駕車成本配置

資料來源 : 美國能源部 DOE, 智璞產業趨勢研究所整理 2022/10

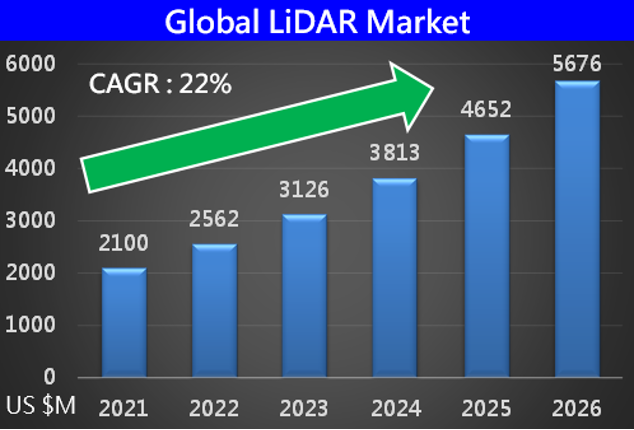

為何我們看好LiDAR。首先,在>L2的自駕車,需要更高的精準度來做預判,光達精準度高於毫米波雷達。過去光達成本非常的高成為導入的最大障礙,但慢慢的成本下降,因此接下來能看到更多的光達出現在自駕車上。雖然Telsa的北美市場捨棄雷達,但去年被證實Telsa自駕車持續有在做光達的測試,大廠賓士也與光達大廠(Luminar)合作導入系統,因此我們依然持續看好。市調機構Yole development預測光達市場如圖4,2023 年全球車用光達市場達360億美金,CAGR達22%。

圖4. 全球光達市場

資料來源 : Yole development, 智璞產業趨勢研究所整理 2022/10

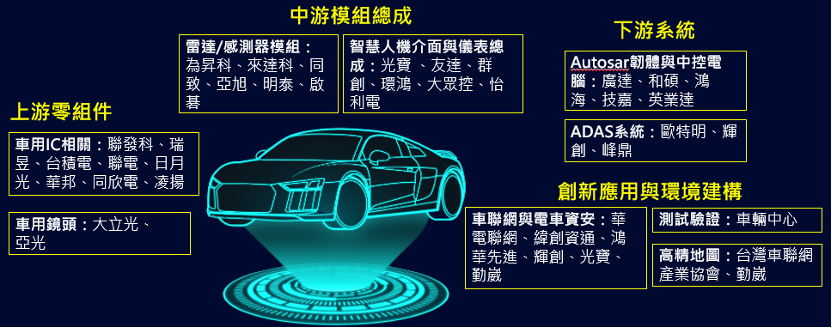

而在整個自駕車產業鏈當中,台灣不論在上中下游都有不錯的表現,如圖5。

圖5. 台灣自駕車相關的產業聚落

資料來源 : 智璞產業趨勢研究所整理 2022/10

上一篇:發表會 | 2023年重要科技趨勢 (中)

下一篇:發表會 | 2023年全球景氣與產業趨勢預測

-For more information, please clickContact Us -

Presentations | Global Climate and Industry Trend Forecast 2023

Presentations | Global Climate and Industry Trend Forecast 2023 Seminar|Key Technology Trends 2023 (Chinese)

Seminar|Key Technology Trends 2023 (Chinese)