PV Industry Trend Report|Photovoltaic Industry Trend(Up)-Renewable Energy and PV Market Trend

As the earth continues to heat up, the climate system undergoes irreversible changes. In April 2022, the United Nations Intergovernmental Panel on Climate Change (IPCC) released its latest report (AR6 WG3), stating that the only chance for mankind to mitigate climate change is to reduce global GHG emissions by more than half by 2030, and that the current global energy source, 83%, is using fossil fuels as a source. The IPCC proposes the following specific measures for governments, including phasing out fossil fuels and switching to renewable energy sources such as solar and wind power; protecting and restoring at least 30% of forests, oceans and other natural ecosystems; protecting and restoring at least 30% of forests, oceans and other natural habitats; and protecting and restoring at least 30% of forests, oceans and other natural habitats. The measures include phasing out fossil fuels in favor of renewable energy sources such as solar and wind power; protecting and restoring at least 30% of forests, oceans and other natural habitats; developing climate-friendly agriculture and food industries; and improving energy efficiency. In order to reduce greenhouse gas emissions, countries around the world have put forward a variety of reduction strategies, major corporations and public and private sector organizations have annual carbon dioxide emissions reduction targets and target dates for achieving net zero emissions, and renewable energy has a low environmental impact of the cleanliness of the characteristics of the majority of the people recognized, therefore, countries are actively promoting the development of renewable energy strategies.

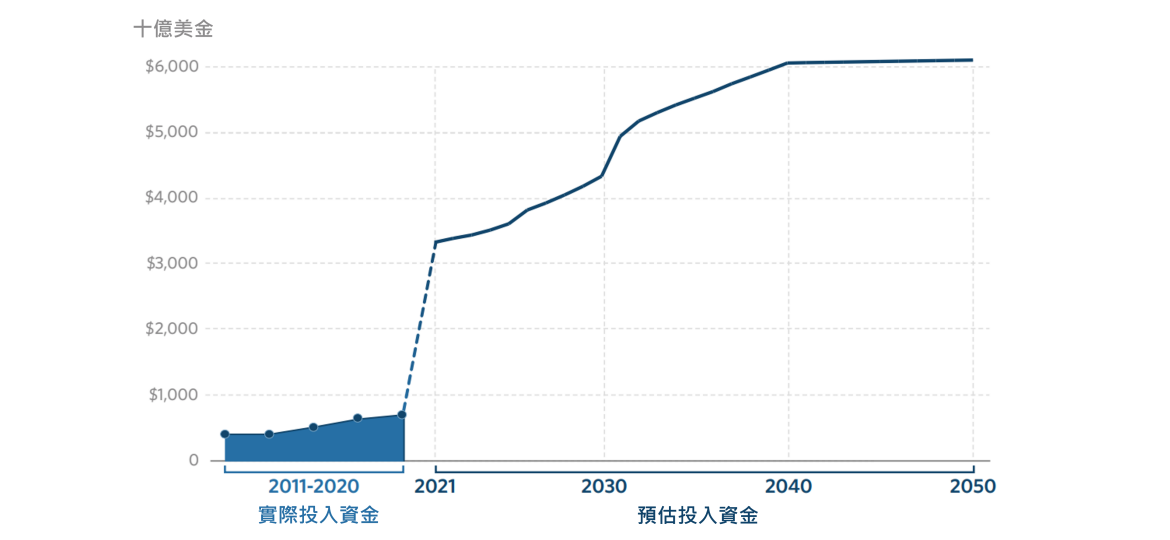

全球氣候金融投資,2040 年將超過6兆美元

“氣候金融(Climate Finance)”指的是用來減緩(mitigation)及調適(adaptation)氣候變遷的資金。依據統計國際能源署(IEA)統計,全球氣候金融2011年到2020年以每年 300億至500億美元的緩慢(YoY 5~8%)速度成長。但在2021年聯合國氣候變化會議上,與會200多國達成《格拉斯哥氣候協定》(Glasgow Climate Pact),內容包括:各國逐年檢視減排目標、逐步淘汰化石燃料、協助貧弱國家抗。COP26也敲定碳市場規則,並釋出數兆美元資金,用於保護森林、建立再生能源設施等遏制氣候變遷的行動。在此之後,2021年全球用來對抗氣候變遷的投資戲劇性成長超過2兆美元。而為了要實現 2050 年淨零排放的目標,將全球暖化控制在1.5°C以內,預估到2030 年時全球每年流向潔淨能源、提升能源效率、零排放運輸、氣候友善農業和保護森林的經費,將增加3至6倍突破4兆美元;2040 年將超過6兆美元,2050 年全球氣候金融投資將維持6兆美元(圖一)。

圖一:2011~2050年全球氣候金融投資預估

資料來源:IEA 2022/8;智璞產業趨勢研究所重製 2022/10

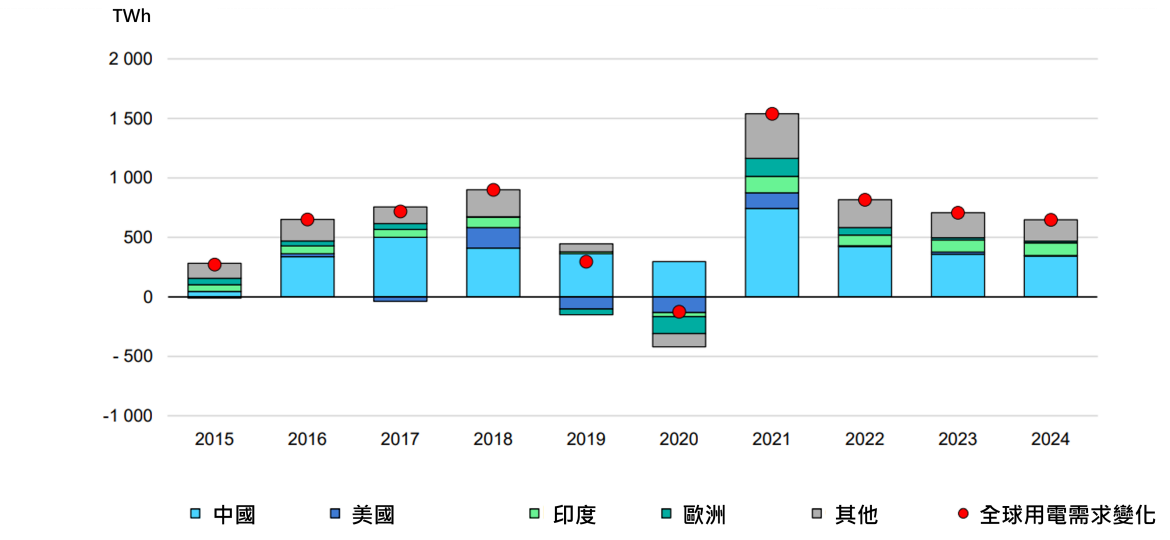

2021年用電需求過度反彈:1. 石化發電增速再創新高。2. 全球太陽能加風力發電佔比達10%

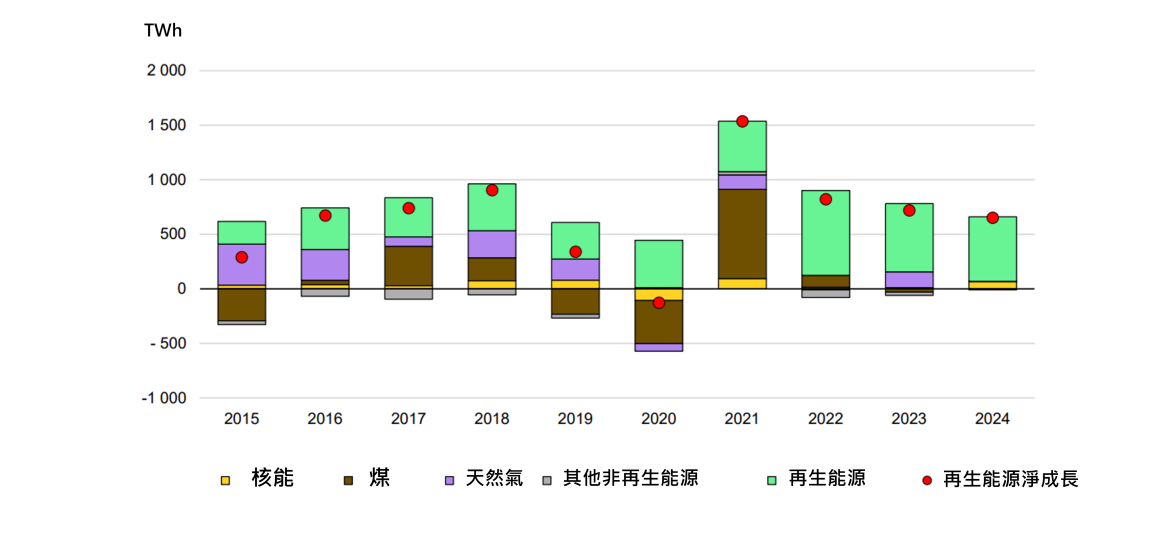

然而在經歷兩年的 COVID-19 大流行造成需求趨緩後,後疫情時代全球經濟過熱導致用電量爆發性成長。根據再生能源平台「21世紀再生能源政策網公司」(REN21)調查,2021 年經濟活動跟夏季高溫導致全球用電需求大幅增加,全年用電量增速再次達到歷史新高(圖二)。新增的能源需求,仍然以石化能源發電佔比最高(圖三),最終造成的結果是二氧化碳排放量再次突破歷史新高。隨後進入2022年,由於俄烏戰爭開打引發了前所未有的全球能源危機和大宗商品短缺,9月初俄羅斯以進行維護作業為由,暫停由北溪1號管線的天然氣輸送,此舉也迫使歐洲各國盡全力尋找替代來源或改採購海運液化天然氣。加上前段所述COP26對於緩解氣候變遷的承諾,全球再生能源的投資已經連續第四年增長,2021年全球各地的投資已達到3660億美元,其中太陽能發電投資為42%,風力發電為39%,而太陽能和風力發電在此年度也首次達到全球共電量10%的里程碑。

圖二:2015~2024年全球各地區用電需求變化

來源: IEA 2022/8;智璞產業趨勢研究所重製 2022/10

圖三:2015~2024年全球各類型發電量變化預估

來源: IEA 2022/8;智璞產業趨勢研究所重製 2022/10

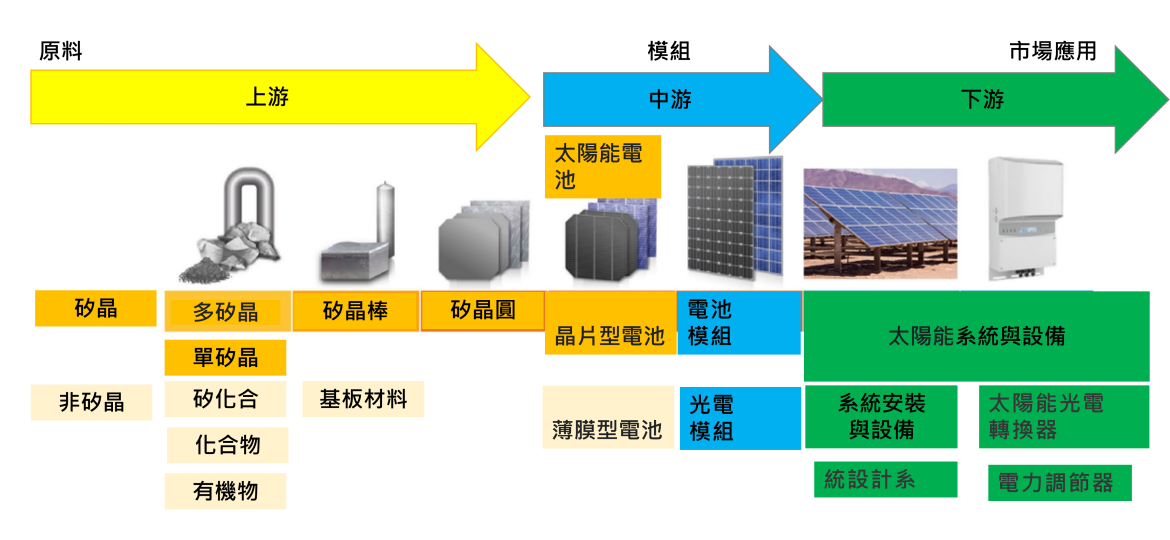

太陽能產業鏈:上游關鍵原料「多晶silicon (chemistry)」80%中國生產,未來若禁止進口,歐美退役工廠將重啟。

太陽能產業鏈分成從上游原料:多矽晶、矽晶棒、矽晶圓、化合物與特用化學品材料等…中游模組:晶片型和薄膜型太陽能電池 (PV solar cell)及光電、及電池模組 (PV module)製造, 下游系統:太陽能系統(PV system)與相關設備的市場應用 (圖四)。

太陽能電池晶片市場以矽為主要原物料,按分子排列結構又可分為多晶矽(Poly-Silicon)與單晶矽(a-Silicon)兩種。矽為地殼中含量第二多的礦物故成本較為低廉,且因矽基半導體的技術較成熟而被廣泛應用於各種積體電路如CPU、記憶體之中。礦石開採之後,利用鎔爐提煉還原成冶金級的矽原料,並且經過鹽酸化、蒸餾化及分解純化等製程,產出多晶矽材料,再利用柴式(CZ)長晶爐以提拉法長晶,逐漸向上提拉為固體的柱狀單晶矽晶棒。之後經過研磨、拋光、切片等等的程序,完成中游客戶所需要的矽晶圓片。中國是太陽能製造重地,目前全球「矽原料太陽能電池」的關鍵原料「多晶矽」 80% 在中國生產,其中 45% 出自新疆大全新能源(Daqo)、新特能源(Xinte)、協鑫集團(Xinjiang GCL)與 East Hope,只有 20% 多晶矽源自非中國地區,這趨勢使得全球太陽能光電供應鏈愈來愈缺乏彈性。今年六月以來中國缺電造成多晶矽斷供,進而導致全球太陽能產業交付延遲和價格飆升的狀況方興未艾。有鑑於此,若美國禁止新疆產品法案正式生效,或美國太陽能原材料溯源規範上路,將導致針對美國市場供給面產生巨大缺口;德國Wacker小型工廠、挪威REC Silicon 已封存的工廠和美國 Hemlock Semiconductor 已經退役的工廠全部都可能重新啟動,以填補失去中國供應鏈造成的供給缺口。

圖四:太陽能產業鏈結構

智璞產業趨勢研究所整理 2022/10

You may have interesting articles:PV Industry Trend Report|Photovoltaic Industry Trend(Chinese)_Industry Chain Distribution and Domestic and Foreign Manufacturers

You may have interesting articles:PV Industry Trend Report|Photovoltaic Industry Trend (Below)_How the U.S. and Taiwan Respond to the Expansion of China's PV Industry

—欲索取更多資訊,請點Contact Us —

Industry Trend Report|Electric Vehicle Demand Drives Taiwan's Automotive Electronics Manufacturers to Connect with the World

Industry Trend Report|Electric Vehicle Demand Drives Taiwan's Automotive Electronics Manufacturers to Connect with the World PV Industry Trend Report|Photovoltaic Industry Trend(Chinese)_Industry Chain Distribution and Domestic and Foreign Manufacturers

PV Industry Trend Report|Photovoltaic Industry Trend(Chinese)_Industry Chain Distribution and Domestic and Foreign Manufacturers