News Release|Intel may eliminate 18A process nodes for foundry customers, leaving TSMC virtually unmatched!

Author: Mr. Lin Weizhi, Executive Vice President, Ji-Pu Industrial Trend Research Institute

News.

According to Tom's Hardware Tech Columnist Anton Shilov, Intel may eliminate the 18A process node for foundry customers and focus more on the 14A process. Samsung may delay or even abandon its 1.4nm R&D program and focus on 3nm and above (5 and 7nm), which has already seen the market, leaving TSMC short-term out of contention.

Ji-Pu Viewpoint:

Conclusion:The fact that TSMC has won again in advanced manufacturing processes should not be news to many people, and its industry leadership and more than half of the market share is a fact that will not change in the minds of many people. However, as TSMC's President Chieh-Chia Wei said at TSMC's shareholders' meeting, TSMC is not afraid of anything but the global economic slowdown. The president made the point clearly.If the economic slowdown affects demand in the next two years and Intel loses a small portion of its smartphone or HPC (Hybrid PC) foundry customers, it could affect the extent of TSMC's advanced manufacturing processes and further impact its growth, and even the configuration of the entire supply chain.

#. IntelAnalysis of the strategic intent of eliminating 18A OEM and switching to 14A.::

Intel's predicament has always been a thorny issue, and during the Pat Gelsinger era, Intel has actively sought to revitalize the company, including the launch of the "Five Node Four Years" program, the release of the IDM 2.0 expansion blueprint, and even tried to utilize government grants + co-investment to externalize the cash pressure (Smart Capital financing cooperation) and other strategies. The new CEO, Lip-Bu Tan, has taken office and made successive moves to revitalize the company. In addition to emphasizing process technology, he has also made significant capital savings, and at the same time, an internal proposal has been circulated requesting the company to stop marketing 18A (1.8 nm) and 18A-P to external customers, and instead shift the focus of foundry work to 14A (1.4 nm). Based on Intel's current capital expenditures and actual revenues, it is estimated that in the coming years, the company will be able to achieve the same results.

Intel will definitely prepare for mobile communication chips such as cell phones, tablets, and other mobile consumer electronics. If 14A gets a customer's favor, I expect it will bring 18A's foundry back to life at the same time (2027 happens to be the next-generation HPC chip, which is the only one that will have a chance to get orders from Fidelity). Financially, if 18A is converted to internal use, Intel's capex for 2025~2026 can be scaled down from $20 billion to around $12 billion or even less. Although it is difficult to maintain confidence in Intel based on the performance of the past five years, and the current yield of 18A is not very good, it is worth celebrating that there is a continuous improvement compared to the previous generations.Therefore, I believe that the mission of 18A is to become a node that must be mass-produced (whether it is its own products or OEM products), and with the 18A's paving the way for the 14A to snatch a relatively sizable number of TSMC's customers.In this big game of semiconductor manufacturing process leader, I don't think Intel can simply or smoothly staged the revenge of the prince, but without external help there is still a chance to survive, which means that if there is external help in the future there is still a lot of possibilities. To paraphrase a famous quote from the late Dr. Stephen Hawking, there is a life, there is hope, and living quietly and waiting for the situation to change before rebounding could be a good outcome for Intel in a bad script.

#. Review of the "Capital Expenditure Trap" and TSMC's Expansion of its Plants

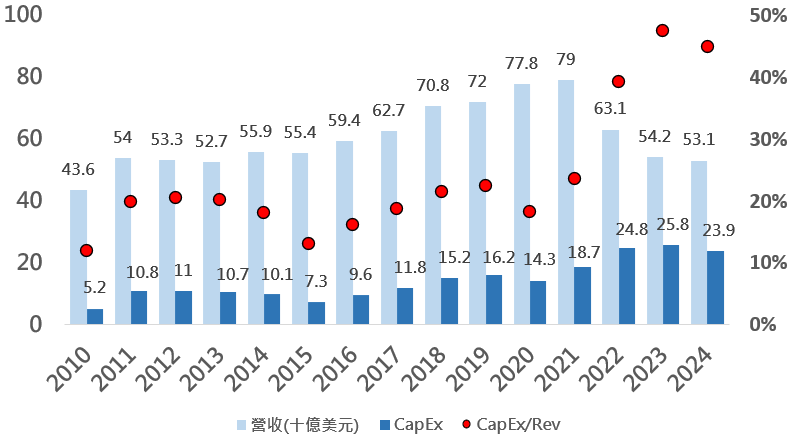

Looking back at the fall of the semiconductor giant Intel, there are bound to be many internal problems have been discussed and analyzed by many people, I think the external problems still come from the product categories are too concentrated (did not seize the mobile communications and AI market), the original target market growth stagnation or even recession and heavy assets due to the delay in advanced nodes, resulting in a decline in capacity utilization → depreciation rates soared → bottoming out of the bottom of the profits → forced to reduce the follow-up CapEx, and finally formed a vicious circle. Intel's 10 nm and 18A both fell into this pit, dragging down the technology rhythm and financial health, the past 15 years of revenue and capital expenditures accounted for Table 1. 2010~2014 ratio of 12%~20%, a normal investment in process replacement; 2015~2018 ratio of 13%~23%, although there is no significant increase in the ratio of 23%~23%). 23%), but encountered 10 nm delay forced 14 nm delayed three generations, CapEx has risen to $US15 bn above. The ratio is close to or exceeds 20 %, but the yield is delayed and depreciation pressure is buried. After 2021, in order to promote Intel 7/4/3/20A/18A at the same time, the "four years and five points" caused CapEx/Revenue to rise from 24 % to nearly 50 %, which is a high-risk section of the capital expenditure trap. In addition, over the past decade or so, the company has failed to capture the two major IC trends of mobile communication and AI HPC, leading to today's situation.

Figure 1 Intel Revenue and CAPEX

Source: Intel; Collated by Ji-Pu Industry Trend Research Institute

Compared to Intel's difficulties, I believe most people who care about the tech industry should be more concerned about whether TSMC will step into the above trap.My answer is: I don't see it now with the rapid expansion of AI demand, but I still need to be careful in the future.The main reasons for not falling into the trap so far are. The main reason for not falling into that trap so far is:

- Continue to capitalize on the expanding market;

- The next step is to finalize customers and co-develop with them, so that each generation has a large customer list (Apple, Nvidia, AMD) and depreciation is rapidly shared;

- Yield rate has been climbing fast and stable, and since N7P, the company has introduced EUV for high-priced machines, with a stable overlapping rhythm.

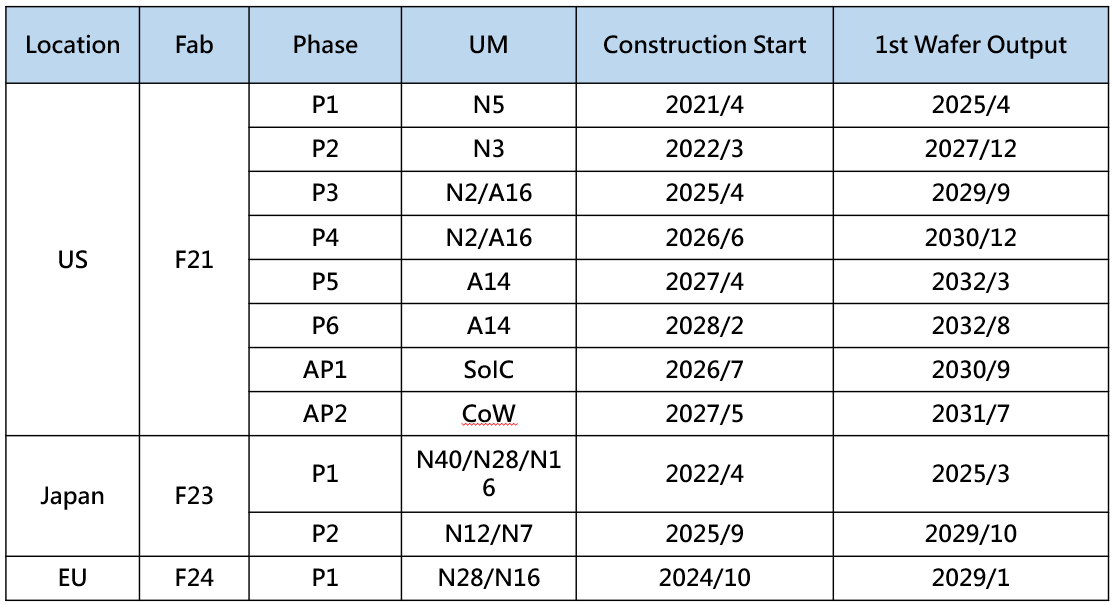

Overall, TSMC is a "high CapEx, but high utilization, high cash conversion" company. However, due to geopolitics and customer satisfaction, TSMC has recently increased its capital expenditure plans on a large scale around the world. Among them, the U.S. is the largest, including the original three phases in Arizona, where the total investment is expected to reach an astronomical figure of $US 160 bn, and the global expansion schedule is summarized in Table 1 below.

Table 1 TSMC Overseas Expansion Information

Source:Internet Information; Organized by Ji-Pu Industry Trend Research Institute

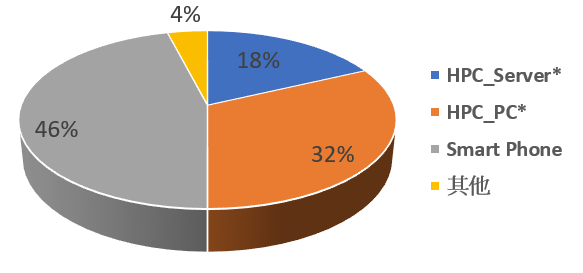

In addition to the F21 P1 (AZ) and F23 P1 (JSMC), which are already in mass production, other official shipments are expected to take place in 2028~2032. Most of the newly expanded production capacity is aimed at advanced processes, and in terms of revenue share in 2024, the share of advanced processes below 7nm (including) is about 70%, and the share of each application area is shown in Figure 2 below. I think Intel is most interested in Apple's IPhone or IPad AP (Application Processor) orders, in addition to the order quantity, the chip area is much smaller than the area of the CPU/GPU, which can speed up the yield curve, faster depreciation is also one of the main reasons. However, due to the past product launch cycle estimation, it takes 24 months to lock in the manufacturing process, and supply errors will delay the entire iPhone cycle, so Intel must come up with ≥60 % yield 14A pilot production wafers in 2026 H2 (or even earlier) before Apple can be convinced; in addition, TSMC in the N3E/A16 PDK (Process Design Kit), package design, and packaging, and the process design kit will be used in the production of the N3E/A16. In addition, TSMC's N3E/A16 PDK (Process Design Kit), packaging (InFO-PoP, etc.) and testing have been deeply integrated for a long time, so how to show Intel's advantage in packaging is also a big problem. If we look at the timeline alone, the chances of getting the IPhone chip should be very low, while the chances of getting the IPad or IWatch chip may be higher. Other customers, Qualcomm / MediaTek flagship cell phone SoC Although the overall volume is not as large as Apple, every time there is a new process in the past, it is inevitable to hear that Qualcomm will go to Samsung to put the chip into trial production as a bargaining chip, due to the habit of multi-source chip, and the area of the smaller, if Intel can be in the cost or discount on the sincerity of the show, there is 5 % If Intel can show sincerity on cost or discount, there will be about 5 % of entry space; Amazon AWS / Google / Microsoft ASIC that has signed a contract in 18A has a volume that is not bad, and there is even a chance of government subsidies in the future, and the customer is willing to share the technology risk, so it is also a customer that is very likely to switch orders. Therefore, if Intel's 14A foundry has achieved some results, there is a chance that a small portion of customer orders will be snatched away in 2027~2028 when the market situation is not yet clear, which will likely make TSMC fall into the above trap.

Figure 2 TSMC's Advanced Processes (7nm and Below) Application Share in 2024

Source: TSMC; Collated by Ji-Pu Industrial Trend Research Institute [*HPC_Server/PC is the estimated value; PC includes tablets, game consoles].

#.How Taiwan's Supply Chain Will Change If Intel-14A Takes 5 % Mobile Communication SoCs::

We remain confident in TSMC's competitive resilience, and since TSMC is currently the only company with a full portfolio of advanced process products, we do not know if there will be an opportunity to technically release some of our orders. However, as Sun Tzu's "The Art of War" says, "I am not afraid that they will not come, but that I will be able to wait for them. Assuming that between the end of 2027 and 2028, 5% of the production of iPhone A-series SoCs, MediaTek's flagship chips in Breguet, or advanced process products such as tablets, game consoles, or AI inference ASICs will be transferred to Intel's 14A node, which will result in about 70,000 to 100,000 1.4 nm wafers per year, and correspond to a loss of revenue of about NT$20 to 30 billion for TSMC. This will result in a revenue loss of about NT$20-30 billion for TSMC. Overall, the scale of the impact is still manageable and not enough to shake TSMC's long-term growth trajectory. However, the ripples that will ensue will require more attention. If customers accept the performance of Intel's 14A products, it will force TSMC to put more pressure on the A16 in terms of pricing and the speed of product launch, so as not to lose the generation lead. In addition, if Intel were to enter the foundry market, the entire supply chain would be shaken. Firstly, the capacity utilization rate of TSMC's back-end outsourcing packaging (OSAT) is bound to be revised downward, and the demand for carrier boards will also be affected by the decline in capacity utilization rate and need to look for other customers; Intel Foveros (Intel's 3D packaging) has its own factories, and U.S.-based customers prefer localization, therefore, Sun Micron (SPIL) and Unimicron may need to set up facilities in Arizona and New Mexico to continue to connect; for material equipment and other components, the supply chain will be affected. In order to continue to receive; for the material equipment and plant plant side of the plant, the current Tier 1 should not be affected by the impact, but may appear to follow Intel-14A, U.S. equipment, material orders are more inclined to land in Arizona, Taiwan's second-tier equipment vendors, if there is no relative subsidy to the situation of increased difficulty in receiving orders.

In terms of technology, if the yield of N2 (GAAFET) is blocked, it will compete with Intel-14A for the first time in the same period [N2 was originally expected to be mass-produced at the end of 2025, but market rumors are mixed, and some analysts have predicted that it may need to be in production until Q1 of 2026, and that the Intel 14A 2027 will be risky to try out, and the mass-production may fall on 2028], and the lead time will be possibly The lead time will probably be shortened to 18 months. Therefore, when I read the column that Intel is again showing weakness, it doesn't mean that TSMC can rest on its laurels. Behind the aura of "one man, one forest" is a higher threshold of technology density, regional politics and capital strength. If TSMC can continue to maintain its process pace and risk-diversification approach, it will be able to avoid repeating Intel's "capital expenditure trap" and continue to lead the world.