上半年產業回顧|剖析全球科技供應鏈,2024年方能迎來產業成長期:AP/ CPU/ GPU大廠

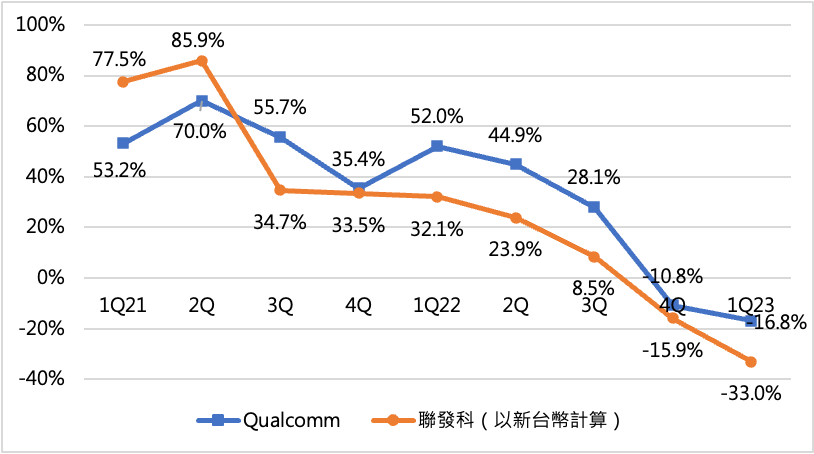

The current market on the global smartphone shipments in 2023 is generally not very optimistic, according to many market research organizations published data forecasts show that sales from only 0.9% growth of 1.202 billion units to a decline of 7%, the total shipments of 1.1 billion units have. The premise of this data still depends on the economic recovery in Europe and the U.S., as well as the economic effects of China's reopening of its borders. In our opinion, given the current global climate, it will take a lot of effort to keep global smartphone shipments flat in 2023. Looking at the revenue performance of the world's two largest mobile chipset vendors, Qualcomm and MediaTek, both companies experienced annual revenue declines in the fourth quarter of 2022, which continued into the first quarter of 2023, although MediaTek's decline was significantly larger than Qualcomm's, as shown in Figure 1. The reason for this is that the inventory level of major handset manufacturers is too high, and their ability to pull goods from the chip industry has declined. In addition, the market share of MediaTek's handset processors in recent years has been significantly higher than that of Qualcomm's, and MediaTek has suffered a more pronounced impact as a result of the one-two punch.

Figure 1. Revenue Growth Rate Change of Qualcomm and MediaTek

Source:Qualcomm & MediaTek Financial Reports; Collated by Ji-Pu Industrial Trend Research Institute

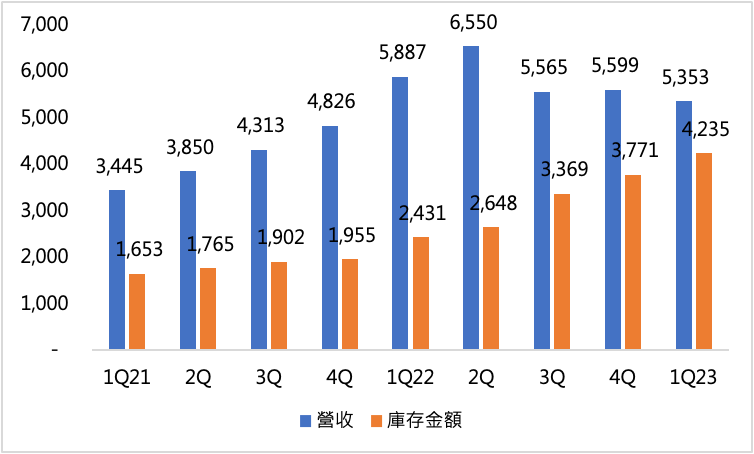

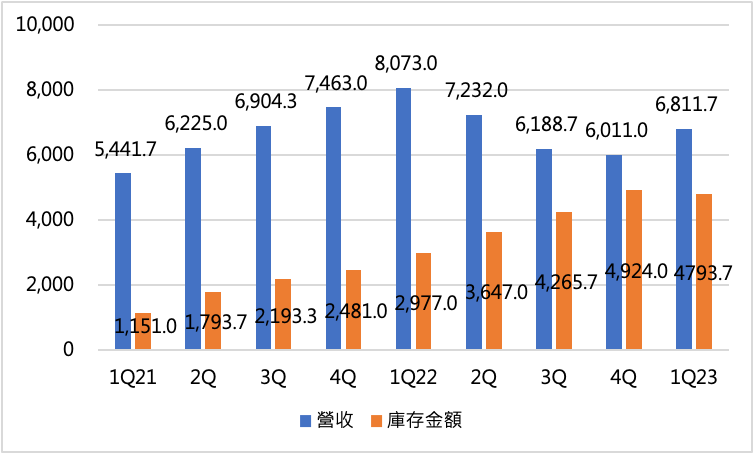

而在庫存金額上,聯發科在2022年第二季達到史上最高,營收亦同,第三季營收雖然對比21年同期仍有成長,但聯發科亦開始調降庫存金額(見圖二)。Qualcomm則是在2022年第四季開始採取行動,相較於聯發科,落後約有半年之久,但以營收層面來說,Qualcomm卻是在2022年第三季達到史上最高(見圖三),其功臣仍是智慧型手機部門,顯然旗艦級與高階市場在2022年第三季末才開始受到終端民生消費力道不佳而動搖。

圖二. 聯發科營收與庫存金額變化 (單位:百萬新台幣)

Source:聯發科;智璞產業趨勢研究所整理

圖三. Qualcomm營收與庫存金額變化 (單位:百萬美元)

Source:Qualcomm;智璞產業趨勢研究所整理

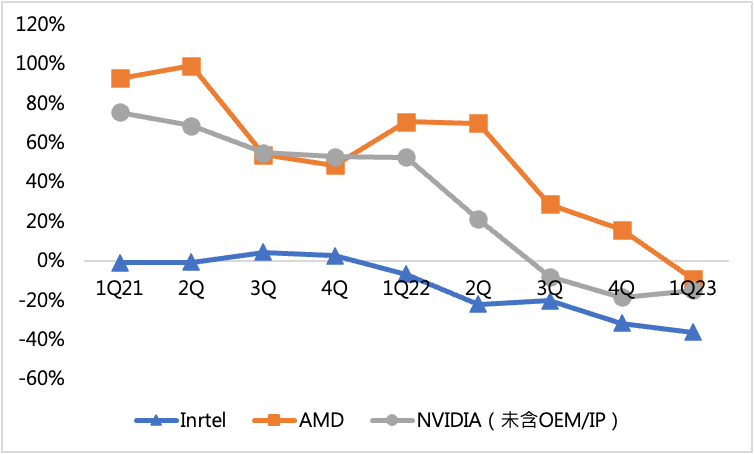

而CPU與GPU大廠,Intel、AMD與NVIDIA在2022年下半年就受到市場逆風的影響,PC與相關的遊戲顯卡產品皆受一定程度的衝擊。其中Intel在2022年全年度的表現相當慘淡,該公司受到先進製程轉進過渡期的影響,在AMD挾台積電先進製程領先的優勢,持續分食Intel在PC與伺服器的市佔率,進入到下半年乃至於2023年第一季,終端消費力道大幅減弱,Intel自2022年第四季至2023年第一季的營收,更是連續兩季出現年衰退達30%(2023年第一季營收年衰退達36.2%)以上的情況,這更是前所未見。NVIDIA與AMD近期在PC市場的表現有類似的情況。

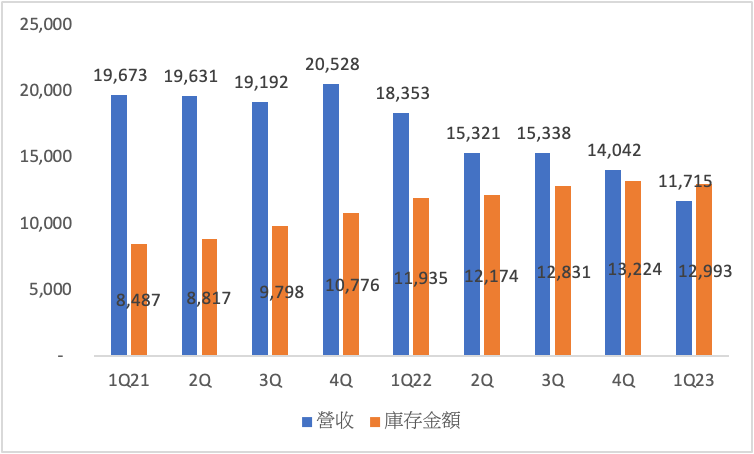

至於NVIDIA在五月中下旬發布新一季的財會季度財報,其整體表現超出市場預期,加上新一季財測也相當出色,故讓NVIDIA股價翻紅。細觀NVIDIA的營收結構,儘管最新一季的財報繳出衰退表現,遊戲顯卡產品線的營收仍持續拖累其整體營收表現,但由於資料中心的表現超出預期,可謂一掃近期全球半導體需求不佳的悲觀氛圍。究其原因不意外的是與近期相當火紅的生成式AI有相當密切的關係,儘管近期美國諸多CSP(雲端服務業者)紛紛採取裁員行動以縮減不必要開的開支來度過全球景氣寒冬,但也因為微軟投資了Open AI,其ChatGPT的應用服務掀起風潮,並帶領新一波硬體需求湧現。使得其他CSP業者不得不有所因應,進一步拉抬NVIDIA在相關AI Server GPU及相關系統方案成長。另一方面,隨著Grace CPU也在五月份進入量產後,可望進一步拉抬Arm base處理器在伺服器市場的市佔率與能見度。而從營收與庫存金額來看,NVIDIA的營收雖然是呈現年衰退,但對比前一季則已有成長跡象,與此同時,庫存金額也已略為下降,顯然NVIDIA也已經著手降低庫存金額,同時也因應生成式AI的強勁需求。

圖四. Intel、AMD與NVIDIA營收成長率表現

Source:Intel、AMD與NVIDIA;智璞產業趨勢研究所整理

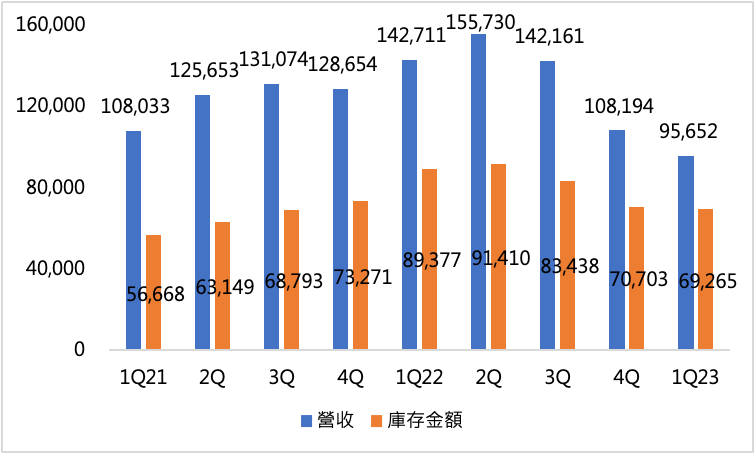

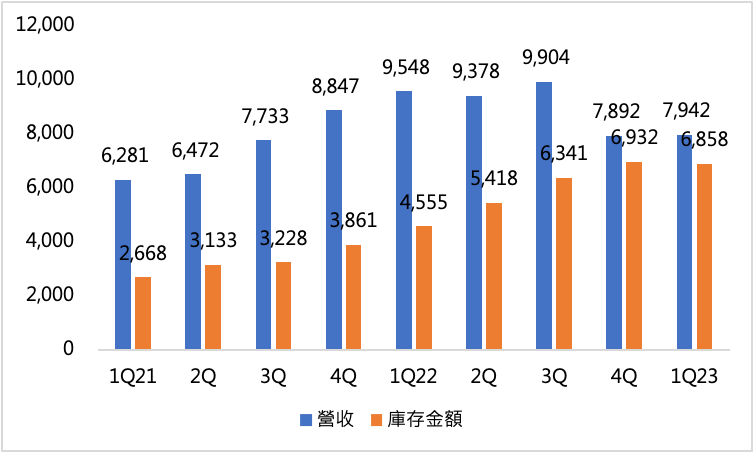

而觀察Intel與AMD在營收與庫存金額的變化,Intel營收明顯出現下滑,但庫存金額幾乎是呈現逐季上升的態勢,到2023年第一季才略為下降,但該季度也是極為少見的,庫存金額高於營收金額的一季,從Intel對於第二季的財測為120億美元左右的水準來看(第一季為117億美元),可以確定Intel仍會受到大量的庫存所苦,如何降低庫存水位將是Intel的當務之急。而AMD的第二季財測約莫落在53億美元左右與第一季相差無幾,但相較於2022年第二季,可以預見年衰退的幅度將進一步擴大,也因此AMD所面臨的情況與Intel並無二致,然而由於AMD本身在完成收購賽靈思的情況下,賽靈思本身的FPGA在許多垂直應用領域仍有一定的成長性,所以應可減緩AMD整體營收不佳的情況。

圖五. Intel的營收與庫存金額變化 (單位:百萬美元)

Source:Intel;智璞產業趨勢研究所整理

圖六. AMD的營收與庫存金額變化 (單位:百萬美元)

Source:AMD;智璞產業趨勢研究所整理

圖七. NVIDIA的營收與庫存金額變化(單位:百萬美元)

Source:NVIDIA;智璞產業趨勢研究所整理