Industry Trend Report|Third Semiconductor Development: Competitive Relationship among Major IDMs (Up)

As we all know, Class III semiconductors have always been a hot topic, and the major IDM companies in Europe, the United States and Japan have basically taken the lead in this field.STMicroelectronics,Infineon,WolfspeedandROHMAccording to the data provided by four IDM companies and third-party research organizations, STM is the leader in the SiC field. On the other hand, with the promotion of the net-zero carbon emission issue, the booming development of electric vehicles and the energy industry, which also promotes the development of power components, ST and the other four companies also intend to further increase the production capacity of SiC components, and the importance of the 8-inch fab in the long term is naturally self-evident. The importance of 8-inch fabs in the long run is self-evident. Unlike the physical characteristics of traditional silicon materials, the wide energy gap feature of Type III semiconductors allows the development of power or RF components that are superior to silicon process components in terms of performance and efficiency. For terminal systems, the use of Type III semiconductors is an irreversible development trend if they want to differentiate themselves from other competitors to create a leading edge. At this stage, most of the semiconductor companies that have invested in SiC and GaN chips are still IDMs from Europe, the U.S., and Japan. Although a few fabless IC designers have also invested in Class III semiconductors, IDMs still lead the overall market in terms of influence.

Recent Developments of Major Manufacturers

I. Infineon

Infineon is one of the three largest IDM companies in Europe, along with ST and NXP, and its overall revenue performance has been even better since the completion of its acquisition of Cypress. At a time when the development of Class III semiconductors was still immature, Infineon was well known in the field of MOSFETs and IGBTs in the early days of the silicon-based process. Infineon's rich experience and foundation in IGBT circuit design, coupled with the mass production of its 12-inch fabs, have helped Infineon to take the lead in the global IGBT field (in the field of discrete components and modules). With the rise of Class III semiconductors and the fact that SiC and GaN are significantly better than IGBTs and MOSFETs in terms of switching frequency and power density, Infineon has been working in this field since the beginning of the development of Class III semiconductors, and is therefore one of the few companies in the world to have a complete range of power switching components (MOSFETs, IGBTs, SiCs, and MOSFETs) at the same time, MOSFETs, IGBTs, SiC and GaN) and RF GaN components at the same time.

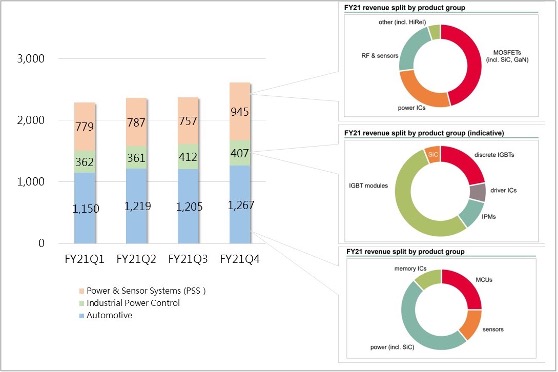

In terms of financial report, Infineon's financial report is based on terminal applications, and Infineon itself is specialized in automotive, power management and industrial automation, so products such as IGBTs and SiCs are scattered in various terminal applications. In terms of Infineon's revenue for the fiscal year of 2021, compared to the same period of the previous year, there is a growth. Infineon has also announced that the revenue of SiC components for fiscal year 2021 will fall within the range of about $200 million, which is a significant growth compared to the same period last year.

Figure 1: InfineonAt fiscal year 2021Major Revenue and Product Share Distribution

Source: Infineon

This shows that Infineon's investment in SiC has already yielded concrete results. As for GaN components, Infineon's strategy is to make its product line widely available in consumer electronics and even automotive OBC (On Board Charger) and DC/DC Converter.

In terms of capacity expansion, Infineon will further consider the possibility of expanding the capacity of its 8-inch fabs in Villach, Germany and Kulim, Malaysia. In the long run, Infineon hopes to further expand the mass production of 12-inch wafers to reduce the unit cost and create a better product price-performance advantage.

II. STMicroelectronics

ST, like Infineon, is one of the few IDMs in the market that owns power components such as MOSFETs, IGBTs, SiC and GaN, etc. ST's revenue for SiC components in 2021 will be around $500 million, and it is estimated that in 2022, it will exceed $700 million. In 2021, ST's total revenue will be $12.76 billion. Although the proportion of SiC component product line in the overall revenue is very low, it can also be seen that SiC has a quite good growth performance. ST also expects SiC revenue to exceed $1 billion in 2023, with 75% coming from automotive electronics and 25% from the industrial sector.

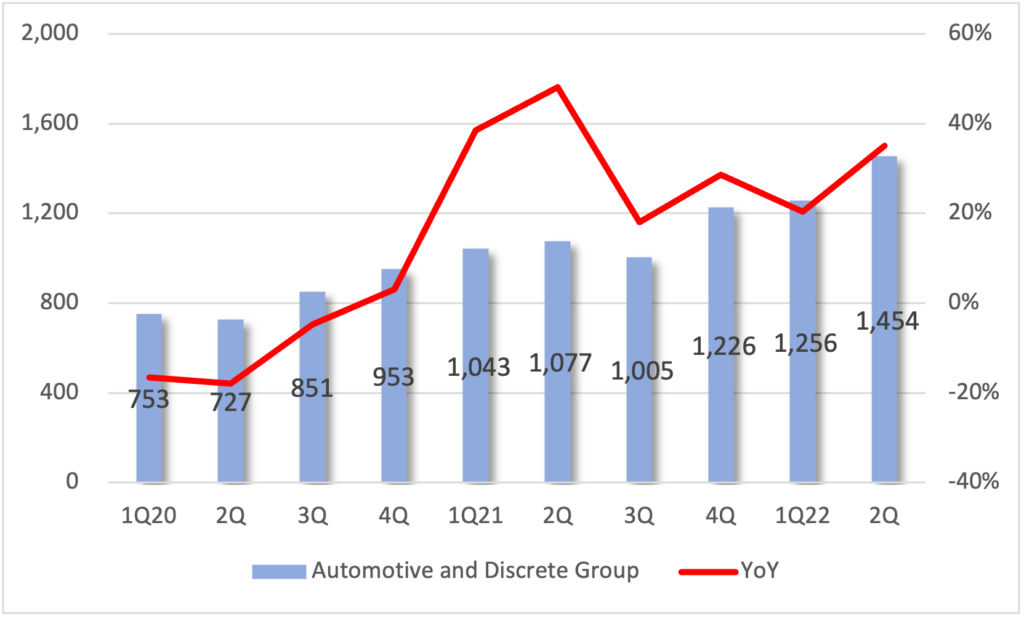

Unlike Infineon's power products, which are scattered in different application areas in its financial report, ST's power component product lines are concentrated in the ADG (Automotive and Discrete Group). According to ST's public information, the revenue of the Automotive and Discrete Group under ADG will be $2.61 billion in 2021, while the revenue of the Discrete Group will be $1.74 billion, both of which have shown significant growth compared to the same period last year.

Figure 2.Revenue Change in the Last Ten Quarters

Unit: millions of dollars Source: ST

In terms of capacity expansion, on the manufacturing side, ST is preparing for mass production of SiC components in eight-inch fabs in Catania (Italy) and Singapore, which is expected to enter mass production in 2023, and it is expected that the capacity in 2025 will be increased to about twice as much as that in 2022. In terms of packaging and testing, the plants in Shenzhen, China and Bouskoura (Morocco) will be responsible. On the other hand, ST is also trying to strengthen the supply of SiC wafer substrates to ensure that the supply of upstream wafer substrate capacity is not in jeopardy, in order to meet the demand of its fabs for mass production of SiC components, according to ST's current estimate, the self-sufficiency rate in 2024 will be able to reach more than 40%.

In the GaN field, the power product line is expected to be mass-produced in Tours' 8-inch fab, with mass production scheduled for 2023, while the RF-related product line will be carried out in Catania's 6-inch fab, which is currently undergoing the production line validation stage.

III. Wolfspeed

Formerly known as Cree, Wolfspeed's product lines at that time were mainly LED and Type III semiconductor product lines and their related wafer mass production, and provided other IDMs with mass production of their own products. Wolfspeed has continued to undergo a strategic restructuring in recent years, and will complete the divestiture of its LED business unit on March 1, 2021, leaving only its Type III semiconductor-related product lines in place at this stage. In the third quarter of the same year, Wolfspeed officially changed its name to In the third quarter of the same year, Wolfspeed officially changed its name to Wolfspeed. Wolfspeed's existing product line mainly consists of SiC power components, GaN on SiC RF components, and SiC wafers, of which SiC wafers are also used by IDMs such as Infineon, ST, and On Semi, and have already signed several years of supply contracts. According to Yole, Wolfspeed is the leading supplier of SiC wafers in the world, with a market share of 62%.

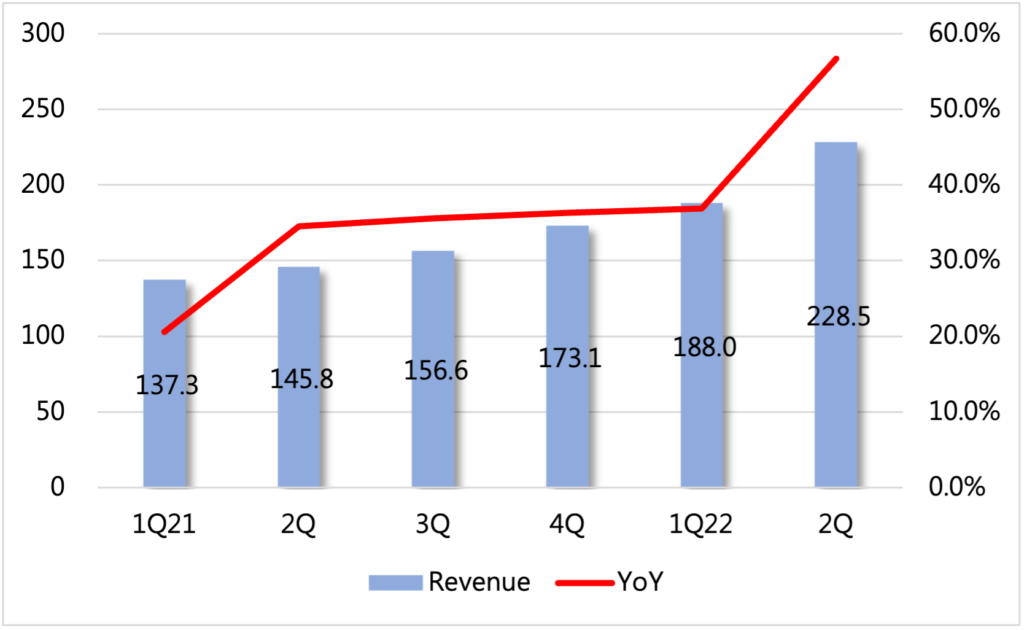

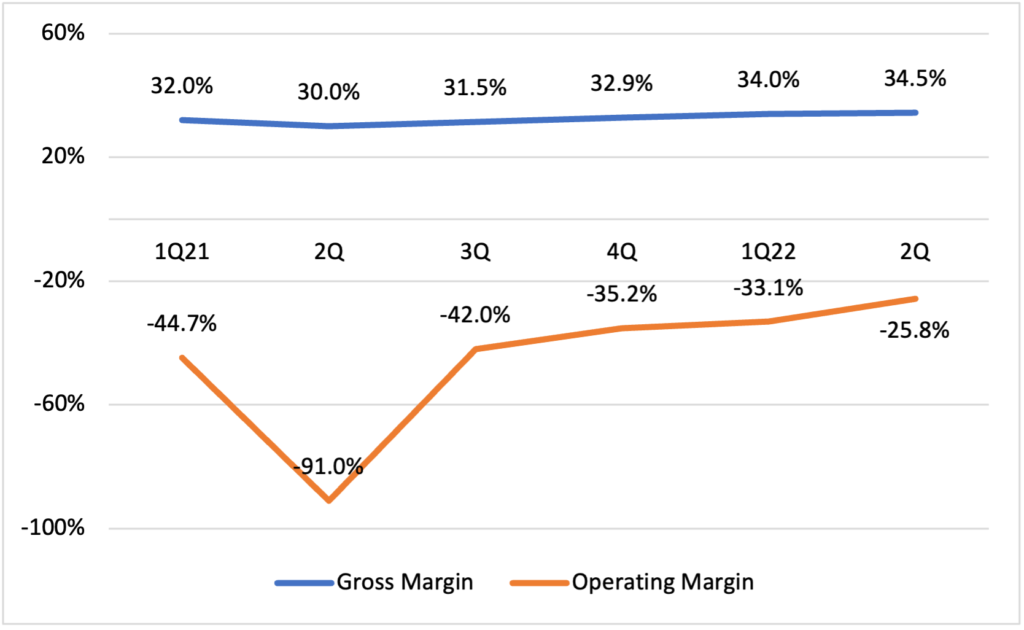

Looking at Wolfspeed's performance in the last six quarters, we can see that Wolfspeed's performance is quite good. While revenue continues to grow, gross margin and operating margin are also on the rise.

Figure 3.Revenue performance for the past six quarters

Unit: millions of dollars Source: Wolfspeed

Figure 4.Gross and Operating Margins for the Past Six Quarters

Source: Wolfspeed

In terms of production capacity, Wolfspeed has already completed the world's first 8-inch SiC device plant in New York, U.S.A., which is confirmed to enter mass production in the third quarter. In addition to this, Wolfspeed also has a 4-inch and a 6-inch plant under its management, which are mainly dedicated to the mass production of SiC power switching devices and Schottky diodes.

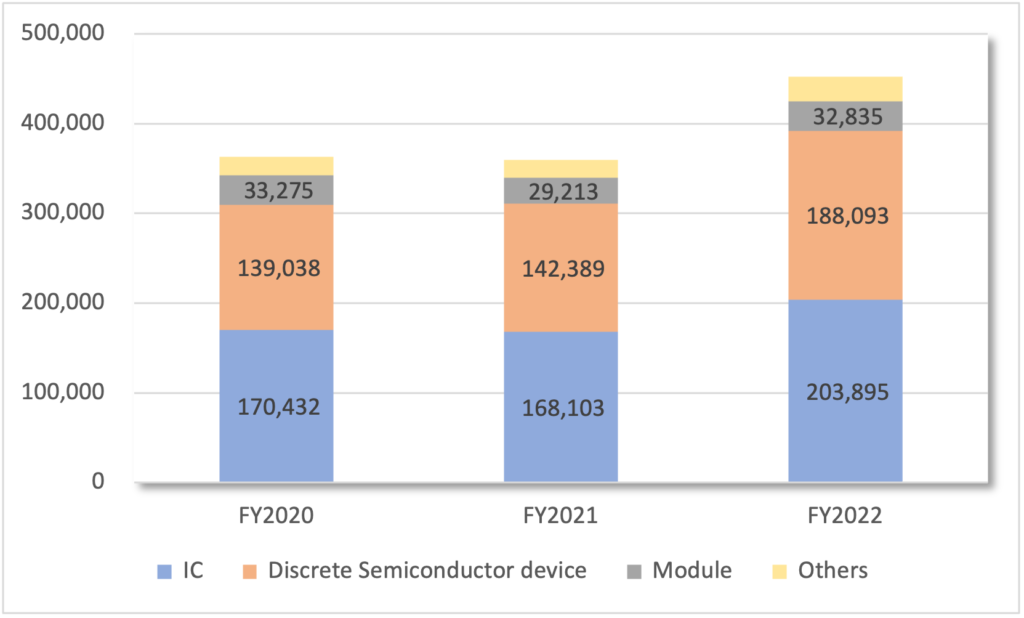

V. ROHM

ROHM is one of the few Japanese IDMs with a wide range of ICs, and similarly, a complete product line of power components, ROHM's revenue is categorized into two types, one according to its IC product line and the other according to the type of application. The former can be divided into general logic ICs, discrete components, and module product lines. Like Infineon and other IDMs, ROHM not only provides discrete components, but also power modules are a source of revenue, only that the proportion of module revenue is quite low compared to that of discrete components.

Figure 5.Product Revenue Performance in the Last Three Fiscal Years

Unit: million yen Source: ROHM

ROHM's development of SiC-related product lines is no less active than that of other European and U.S. IDM companies, such as SiC MOSFET product design in recent years, all major manufacturers have changed to a trench structure, ROHM as early as 2015 has been ahead of the introduction of other industry players, the mass production of all-SiC power modules, also reached in 2012, you can see that the company has a certain amount of strength in the field. We can see that the company has certain strength in this field. On the other hand, ROHM's strategy for supplying SiC wafers is the same as Wolfspeed's. In 2009, ROHM acquired SiCrystal AG in Germany, whose main business is to provide SiC wafers. In terms of mass production, ROHM's six-inch plants in Chikugo and Miyazaki, Japan, will be used for mass production, and it is expected that an eight-inch plant will be used for mass production of SiC components by 2025.

You may have interesting articles:Industry Trend Report|Class III Semiconductor Development is Rising Competitive Relationship among Major IDMs_Next

-For more information, please clickContact Us -

Industry Trend Report|GaN Industry Chain Competitiveness

Industry Trend Report|GaN Industry Chain Competitiveness Industry Trend Report|Third Semiconductor Development: Competitive Relationship among Major IDMs (Next)

Industry Trend Report|Third Semiconductor Development: Competitive Relationship among Major IDMs (Next)