June_Pharmaceuticals|U.S. Biosafety Act: CDMOs are grabbing the business opportunities

After the COVID-19 epidemic, drug shortages, pressure on drug prices and geopolitical risks in the supply chain continue to emphasize the importance of flexible manufacturing and stable supply chain, and raise the awareness of risks in the biopharmaceutical CDMO (Contract Development and Manufacturing Organization) supply chain distribution. The new version of the BIOSECURE Act is gradually building up the defense of biopharmaceuticals and raising the uncertainty of the supply chain! The bill mainly prevents the outflow of core data of U.S. biopharmaceutical research and development, and restricts the dealings with Chinese biopharmaceutical companies, so will the U.S. biopharmaceutical industry and China's CDMOs embark on the path of decoupling? Has become the international CDMO continued focus of attention, the bill seems to let the European, Korean, Japanese and Taiwanese CDMO manufacturers smell the CDMO re-order business opportunities, the future will certainly lead to changes in the CDMO supply chain landscape.

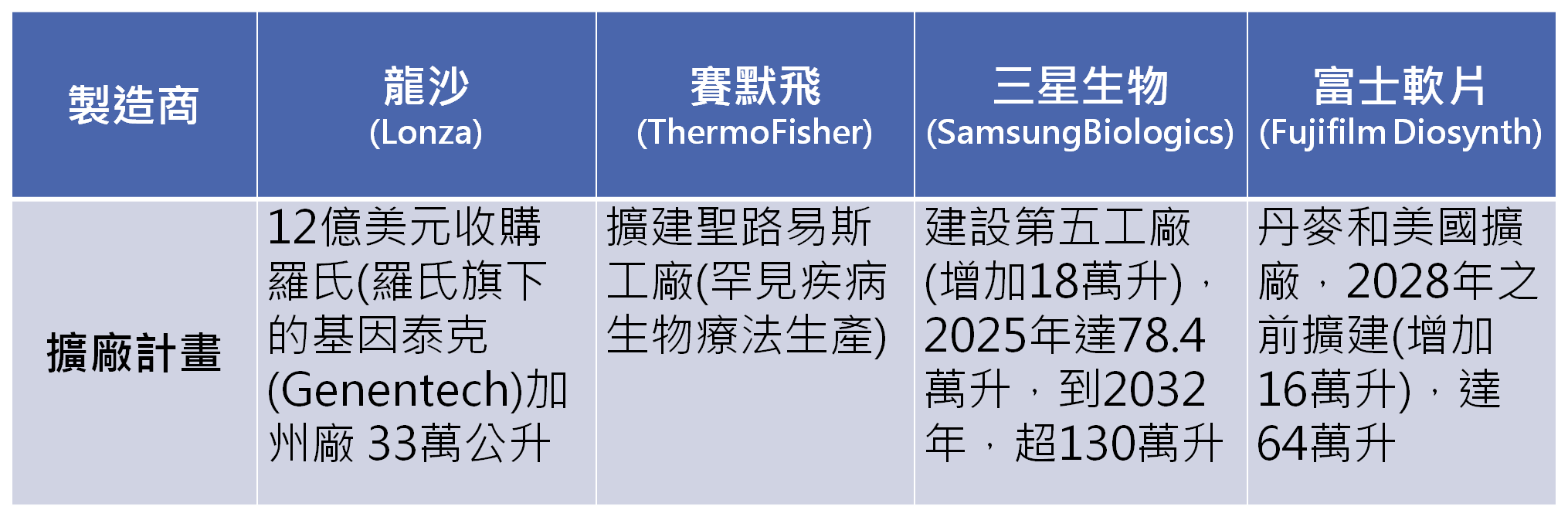

Global BiopharmaceuticalsCDMOStronger outlook, avoiding the risk of failure in new drug development and focusing on production margins According to Nova One Advisor (2024), the global biopharmaceutical CDMO market will reach US$146.29 billion in 2023, and is expected to grow 1.75 times to US$257.05 billion in 2031, with an annual compounded growth rate of 7.3%, which is still higher than the global pharmaceutical market's annual compounded growth rate of 5.7%.The growth driver of CDMO comes from the fact that the cost of establishing and operating pharmaceutical facilities is very expensive. As the operating cost of establishing pharmaceutical facilities is quite expensive, the trend of division of labor in the biopharmaceutical industry chain is becoming more and more obvious, and large pharmaceutical companies are focusing on allocating their operating resources to new drug R&D and pharmaceutical marketing, which are the most value-creating areas, instead of manufacturing, due to the increasing difficulties in new drug development and the trend towards technological and manufacturing complexity, from the mainstream small molecule chemicals in the past, towards complex novel small molecule drugs, or high-level biologics with complicated manufacturing processes. Complex manufacturing processes for biologics, such as new antibody/protein drugs, new ADC drugs, and new cellular and gene therapy drugs such as CAR-T and mRNA, have made large pharmaceutical companies more willing to establish strategic alliances with CDMOs that specialize in manufacturing, and to outsource mid- and back-end drug development and mass-production manufacturing in order to lower the manufacturing costs, instead of building their own factories; and for those who are engaged in the research and clinical development of candidate drugs, and in the manufacturing and sales of drugs, there is a trend towards complexity in technology and manufacturing. For innovative small and medium-sized new drug companies whose core competency is drug candidate research and clinical trial promotion, most of them lack the spare capacity to invest in manufacturing equipment due to limited capital, and therefore rely more on CDMOs that can work across various pharmaceutical technology types and specialize in clinical projects to reduce development costs. The commercial advantage of the biopharmaceutical CDMO industry is that it focuses on production margins, earns money from OEM services, avoids the huge risk of new drug development failure, enters from the early stage of the new drug R&D value chain (CDMO OEM for new drugs in clinical projects), and binds front-end services to gain a larger customer base, so as to expand the opportunities for receiving orders from commercial mass production (commercial-scale CDMO) in the future, and commercial mass production of CDMOs has the potential to expand on a large scale. Growth and stable profits are usually achieved through long-term orders of 6 years or more. Currently, most international CDMO manufacturers are investing in new facilities, new technologies, or introducing advanced and high-efficiency manufacturing through capital expenditures or acquisition deals in order to realize rapid expansion. In view of the huge growth opportunities arising from the accelerated de-neutralization of the U.S. Biosafety Act, as shown in Table 1, Lonza, Thermo Fisher Scientific, Fujifilm Diosynth and other major international CDMO companies have already begun to lay out their plans for the expansion of U.S. factories, and the business opportunities for expanding their production capacity come from the following sources: (1) filling up the business opportunities arising from the release of production capacity, such as the release of production capacity from the market; (2) expanding the production capacity of CDMOs; (3) expanding the capacity of CDMOs; and (4) increasing the capacity of CDMOs. The business opportunities of expanding production capacity come from a. Filling the business opportunities of releasing production capacity in the market, such as seizing the supply chain of China discharged by the Biosafety Act, such as the WuXi system (WuXi Biotech + WuXi Kande), as well as the production capacity vacancies released by the acquisition of Catalent by Novo Holdings A/S. b. The business opportunities of outsourcing trend of lowering the cost, CDMOs are the important partners for commercial mass production of large pharmaceutical companies, and under the premise of the continuous fermentation of the strategy of lowering cost outsourcing, CDMOs are the key partners for large-scale commercial mass production of large-scale pharmaceutical companies. Under the premise of continuous fermentation of the outsourcing strategy, the outsourcing penetration rate will continue to expand from the original 30% to 40% in 2026. For example, Samsung BioSystems and Fujifilm are continuing to strengthen the commercial mass production manufacturing opportunities for the world's top 20 pharmaceutical companies; iii. Business opportunities arising from the increase in the demand for emerging therapeutic methods and the development of innovative medicines; CDMOs have been expanding the content of their services from the value chain of new drug development, and have gradually become the new driving force for technological innovation. CDMO has expanded its services from the new drug development value chain and gradually become a new driver of technological innovation, such as new innovative drugs such as ADC, CAR-T, mRNA cells and gene drugs, etc. Emerging therapeutics rely on highly specialized and diversified types of pharmaceutical technologies, and even early clinical front-end participation, to satisfy the needs of innovative new drug companies in the areas of development, manufacturing services, regulatory supervision, and the pressure of commercial competition, etc. CDMO has also been involved in the development of new drugs and innovative drugs. Table 1: Expansion Plans of International CDMO Plants Source: Organized by Ji-Pu Industrial Trend Research Institute. CDMOTaiwan and U.S. pharmaceutical companies are highly connected, and high-end manufacturers are competing in the international arena. CDMO biotech-pharmaceutical competition, whether it is the original drug international manufacturers commissioned OEM, new drug commissioned OEM, famous drug commissioned OEM, or biosimilar drug commissioned OEM, or cellular and genetic products commissioned OEM, etc. OEM competition and supply chain maintenance will tend to be more heated. the three keys to the development of CDMO are the innovative and advanced manufacturing technology capability, the advantage of cost and speed of scale, and supply chain. As the trade war between China and the U.S. continues, the relevant U.S. drafts (or decrees) have blocked cooperation between China and the U.S. in the biotech-pharmaceutical field, and the level of impact has been expanding step by step. Under the headwinds of orders received by Chinese CDMO enterprises, Taiwanese CMDOs are also expected to welcome the opportunity to get a share of the pie. At present, Porui and TAYA have inserted themselves into the U.S. by way of a merger and acquisition model, and Yungsin, Polaris Pharmaceuticals - KY, TEFL, HANDA, and EWI, etc., have already established supply chain in the United States. With the trend of comprehensive efficiency brought about by the integration of the international CDMO supply chain, how Taiwan companies can maximize their competitive advantages in terms of R&D personnel costs (about 1/3 of the U.S.), expertise in new drug delivery technologies, high-end innovative drug development and manufacturing, and cost control of complex manufacturing processes will also affect the future business opportunities for Taiwan companies in terms of order intake. -For more information, please contact us at

June_Regenerative Medicine|Regenerative medicine outlook is promising, regenerative medicine law helps Taiwan factories to upgrade

June_Regenerative Medicine|Regenerative medicine outlook is promising, regenerative medicine law helps Taiwan factories to upgrade July_New Drugs|ADC Gold Rush Continues to Grow

July_New Drugs|ADC Gold Rush Continues to Grow