June_Half-Year Industry Review|Dissecting the Global Technology Supply Chain for Industry Growth Until 2024:Taiwan IC Design Co.

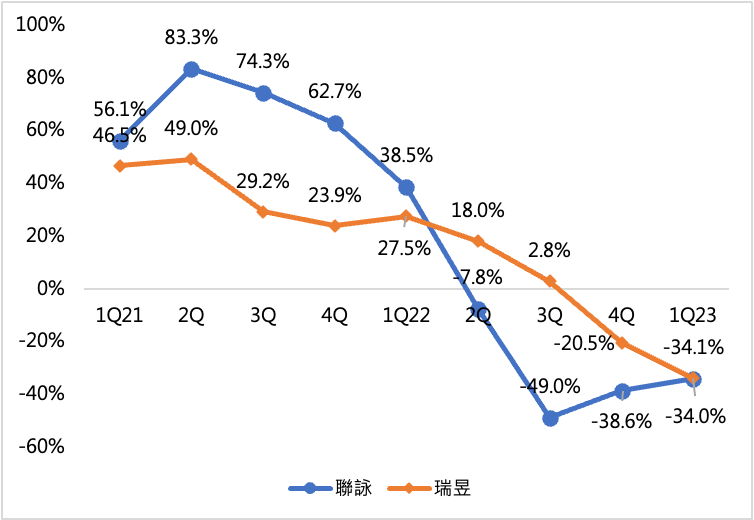

In addition to MediaTek (see previous post for a discussion of AP/CPU/GPU manufacturers), Uniwing and Reynolds are the second and third largest IC designers in China. Since the second quarter of 2022, due to the sluggish global demand for consumer electronics, the sales of display applications are not good, there is a slight downtrend, to the third quarter can be said to show an avalanche of decline, in the past in the gross margin could once be maintained at 50% above and below, but in the first quarter of 2023, only 41.9%. The situation is less serious, until the fourth quarter of 2022 before the annual decline in the situation, but to the first quarter of 2023, ReneSola completely unbeaten by China's weak economic situation, poor demand for network communications, the quarterly annual revenue decline also exceeded 30%, gross margins also plummeted to 43.1%, as shown in Figure 1.

Chart 1 Annual Revenue Growth by Quarter for Unitech and Rexchip

Source:Union and Reynolds; Collated by Chi-Pu Industry Trend Research Institute

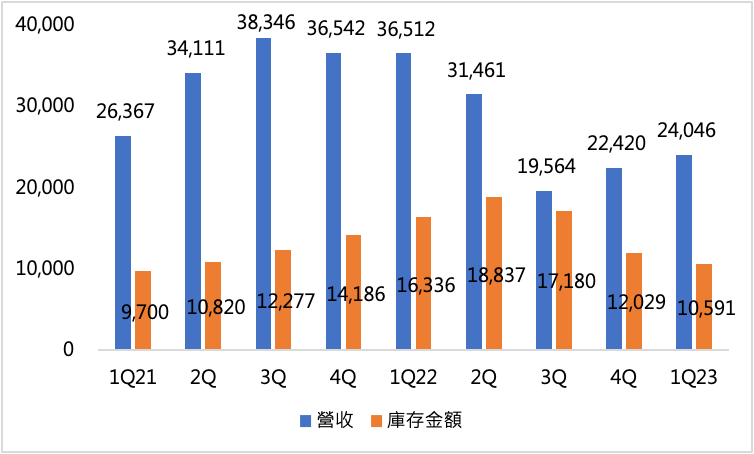

聯詠以顯示器DDIC(驅動IC)為主要產品,此類產品受到市場波動、景氣影響等因素相對劇烈。根據市調機構發布的報告,2023年DDIC 整體需求預測下修至 8.44 億單位,年增長也從之前的 2% 下調至1%。此外估計2023年LCD DDIC需求將同比增長4%。智能手機DDIC需求將持續下降,而AMOLED智能手機DDIC需求將恢復增長。預計 2023 年 DDIC 總需求將與 2022 年持平,到 2024 年需求將恢復增長 6%。隨著許多大型面板應用越來越多,DDIC 需求將持續超過3%的增長到2027 年。從兩年前的晶片短缺,IC design與代工廠簽屬LTA;接著面板供過於求,面板廠為了穩定價格因此控制了產能,導致DDIC庫存消化非常緩慢。因此我們發現面板製造商的 DDIC 庫存在 2022 年Q3度增加了15~25%。

觀察全球主要DDIC產品應用的市佔率,聯詠在2022年大致是各領域的第一名,大面積DDIC 市佔率23.9%、手機/平板DDIC市佔率26.4%、車用面板DDIC市佔率27.5%、LCD TDDI市佔率20.2%。因此在面板需求明顯下降時,聯詠在營收表現上幾乎是呈現雪崩式地衰退。進一步觀察,其衰退幅度已逐漸縮小,從2022年第三季的年衰退49%,到2023年第一季已進展至34.1%。觀察庫存情況,聯詠的庫存金額在2022年第二季來到歷史新高的188億新台幣的水準,該季度營收也開始出現微幅下滑,年衰退為7.8%;從庫存金額的變化來看,聯詠顯然相當積極去化手上的庫存,自2022年第三季開始,其營收已經自谷底的195億新台幣逐季上揚,庫存金額也開始下降,尤其進入到第四季,庫存金額更一口氣降低至120億新台幣的水準,2023年第一季更降低100億。估算庫存天數(DoI),目前聯詠已回到業界普遍認定的健康水位(<4 weeks),此表現優於市面上許多DDIC公司。

圖二 聯詠營收金額與庫存金額變化 (單位:百萬新台幣)

Source:聯詠;智璞產業趨勢研究所整理

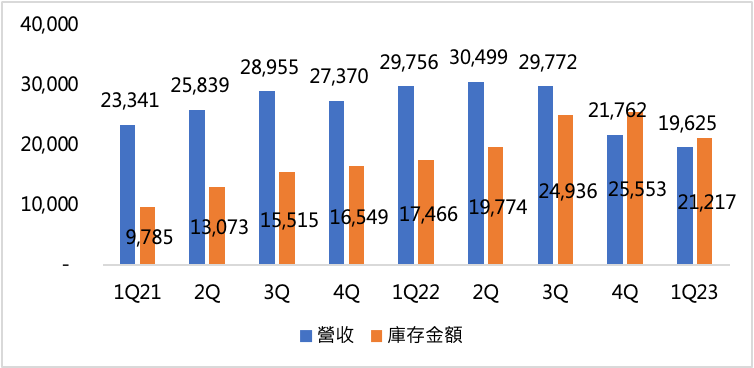

而瑞昱的營收波動截至目前為止,雖然不像聯詠那般劇烈,但在庫存金額上,自2022年第四季開始,已經連續兩季超過營收,但瑞昱官方也說明預計第二季營收表現將優於第一季,也因此,第一季預計將是瑞昱的營收谷底時期,進入第二季,受惠於如Wi-Fi、乙太網路與音訊晶片等需求回溫,其營收預計將有所成長,下半年整體表現將優於上半年。這可能也顯示出瑞昱雖然受到市場景氣衝擊,但影響幅度不若聯發科與聯詠來得大,因應其下半年需求,故在庫存上有所準備,讓2023年全年度營收得以保持成長態勢。

圖三 瑞昱營收金額與庫存金額變化 (單位:百萬新台幣)

Source:瑞昱;智璞產業趨勢研究所整理

June_Half-Year Industry Review|Analyzing the global technology supply chain, the industry growth period will only come in 2024: AP/ CPU/ GPU makers

June_Half-Year Industry Review|Analyzing the global technology supply chain, the industry growth period will only come in 2024: AP/ CPU/ GPU makers June_Half-Year Industry Review|Analyzing the Global Technology Supply Chain, 2024 will be the Year of Industry Growth: Foundry and TSMC

June_Half-Year Industry Review|Analyzing the Global Technology Supply Chain, 2024 will be the Year of Industry Growth: Foundry and TSMC