光通訊專題|插拔式光通訊模組市場與技術發展概況(上)

Author: Mr. Lin Weizhi, Executive Vice President, Ji-Pu Industrial Trend Research Institute

With the launch of OpenAI's O-series models, DEEPSEEK's R1, and xAI's Grok3 and other next-generation generative AI technologies with logical reasoning capabilities, we believe that the demand for high-performance computing (HPC) and AI training has not been reduced by the slowdown in the rate of Pre Training enhancements, but rather has increased due to the launch of new AI models that have allowed the advancement of AGI [general-purpose AI] to see the light of day. On the contrary, the introduction of new AI models has raised the demand for AGI (Generalized Artificial Intelligence). We also believe that this trend will further drive the development of optical transmission technology. Unlike traditional computing models, AI training and reasoning processes involve

根據市場研究機構 Yole Group 於 2024 年 5 月發布的最新報告,2023 年初,由於資料中心需求減少和資本支出放緩,光通訊模組市場前景黯淡。然而,從 2023 年 3 月開始,Google、Amazon 和 NVIDIA 等超大型客戶的推動下,800 Gbit/s 光通訊模組的需求激增,帶動訂單和出貨量大幅增長。2023 年晚些時候,Microsoft 和 Meta 也增加了對 400 Gbit/s 光通訊模組的需求,反映出人工智慧驅動的市場正在不斷擴大,2024年隨著新款 AI 伺服器開始採用 800 Gbit/s 光通訊模組,全球市場規模將同比增長將近30%,達到 138 億美元,供應商陸續透過提高產能和確保供應鏈供給無虞,來為 800 Gbit/s 和 400 Gbit/s 收入的大幅增長做好準備。時序進入2025年,到目前(2月)為止尚未明確聽到有CSP企業下調CAPEX的聲音,以此態勢預估接下來的光模塊進步將會從800G持續移動至1.6T移動。根據最新市場預測資料,目前矽光技術雖然已逐步成熟,但採用Si Interposer的CPO方案仍面臨成本、製程技術與良率等挑戰,普及化大規模導入可能還需要數年的時間,因此我們預估2025年還是以傳統光模塊為主軸。

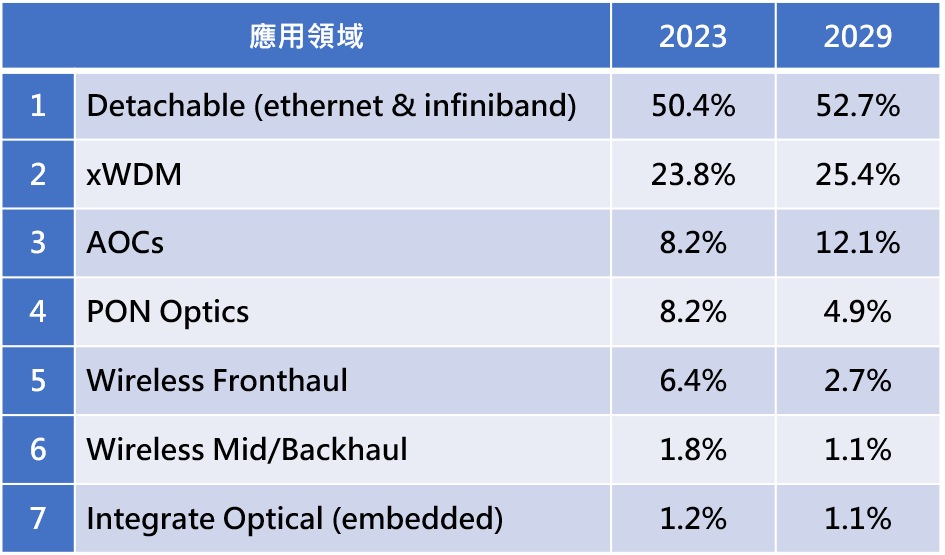

依據調研機構顯示光通訊模組市場到2029 年將達到 224 億美元,這是由於雲端運算廠商和電信運營商對 400 Gbit/s以上(含)高速率光通訊模組的高需求所致。現階段,光通訊模組的應用市佔率如表 1 所列,前三大應用領域為乙太網路 (Ethernet) 與無限頻寬 (Infiniband) 網路的可插拔產品、波分複用 (xWDM) 與主動光纖 (AOCs),其中主要用於資料中心的可插拔產品市佔率超過 50%。值得注意的是,NVIDIA 推出的 GB200 NVL72 伺服器機櫃中,內部訊號採用高速背板連接器的銅纜互連,其優勢在於價格低廉且因不涉及光電轉換而具有較小功耗。只有在超過 72 顆 GPU 的跨機櫃或伺服器叢集間訊號連接時,才會使用光通訊模組。由於其他 AI 處理器廠商開發的伺服器也可能採用相同作法,預期該趨勢會部分抑制光通訊模組需求的增長幅度,但應不至於改變光通訊在資料中心訊號傳輸中的主流技術地位。

表1、光通訊模組的應用領域之市場占比

資料來源 : Yole Group