July_Optical Communication|Optical Communication Module Market Analysis(Up)

Last October, we published a series of silicon photonics and co-packaging special reports. As AI's demand for hardware computing power continues to rise, and so does the demand for data transmission, both the market dynamics of the 800G volume release and the trend forecast of optical-in-copper-out discussions indicate that data transmission is still the focus of the market, so this month's special report focuses on the current situation of the optical communication market update. At present, Datacom and Telecom are the two major end-use markets for optical communication modules. In recent years, the rapid progress of generative AI technology has attracted more and more vendors to invest in building data centers to train AI models.

光通訊模組產業鏈大致可分為上游的零組件設計製造商、中游的模組製造商與下游的終端應用業者等三部分,它的零組件主要有數位訊號處理器(DSP)、雷射源驅動器(LDD)、光訊號發射器(TOSA)、光訊號接收器(ROSA)、轉阻放大器(TIA)、限制放大器(LA)、時脈與資料恢復器(CDR)、微控制器(MCU)、電路板、機殼與連接器等。下游的終端應用業者多為雲端資料中心(CSP)、電信之設備製造商與運營商。以往光通訊模組設計與製造業是由歐、美廠商主導委託代工,近10年內中國業者憑藉低成本優勢迅速擴大市場占有率而居於領導地位,根據市場研究機構LightCounting的報告指出2023年全球前十大光通訊模組供應商中已有7家中國公司,包括第一名的中際旭創、第三名的華為、第五名的光迅科技、第六名的海信寬頻、第七名的新易盛、第八名的華工正源、第九名的索爾思光電,如表1所列。

表1、2022、2023年全球前十大光通訊模組供應商名單

資料來源 : LightCounting

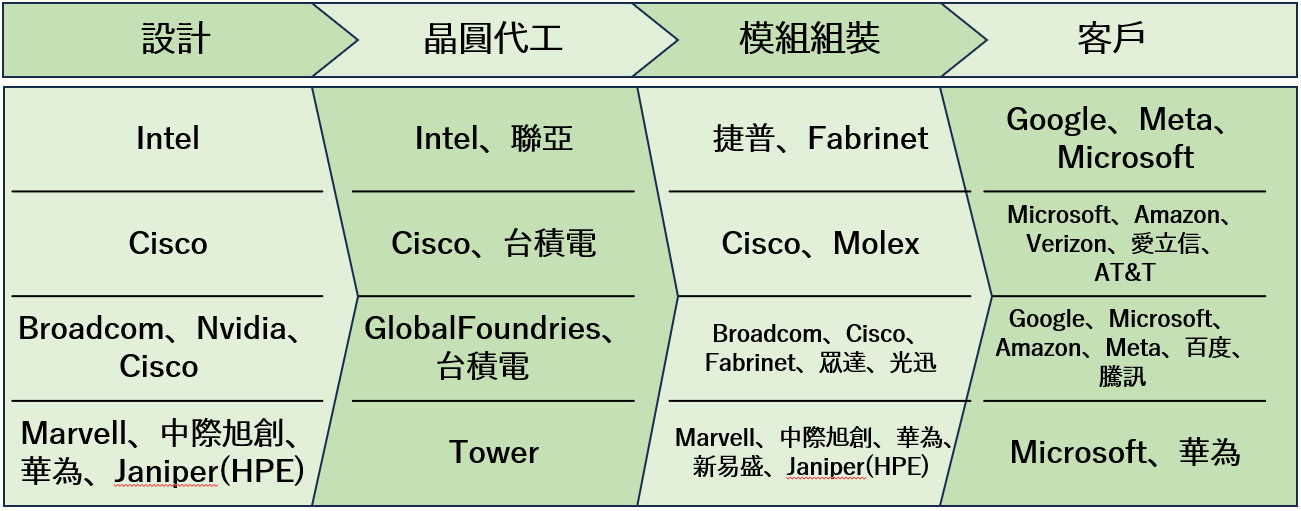

目前通訊產業鏈從上到下都在積極瞄準矽光子相關應用,雖然目前整體滲透率不高,以2023年數據中心的收發器為例,矽光子大約占比5%。然而對資料傳輸市場而言,其低功耗、低延遲與大頻寬等強硬優勢,矽光子將會是一必然的解決方案。由於目前滲透率偏低,供應鏈多為互相研發合作、小批量代工、測試驗證,待未來將隨需求上升朝向專業分工,依供應商分類之供應鏈如下圖1。

圖1 矽光子供應鏈

Source: Organized by Jipu Industrial Trend Research Institute.

May_Sora|OpenAl Sora Technology and Advantages(Next)

May_Sora|OpenAl Sora Technology and Advantages(Next) July_Optical Communication Market|Optical Communication Module Market Development Analysis(Next)

July_Optical Communication Market|Optical Communication Module Market Development Analysis(Next)