February_Self-driving ICs|Global Self-driving ICs Market Analysis(Part2)

Market research firm Counterpoint estimates the ADAS processor market size to be US$30 billion in 2030, with a CAGR of 26.2% from 2025 to 2030. ADAS processors for Level 1 and 2 will become the mainstream products in the market from 2024 due to the decreasing cost of sensors such as cameras and millimeter-wave radar. Because of the need for more computing power and faster response time, it is not expected to be replaced by a large number of Level 3 and 4 processors in the short term. the ADAS processor market entry threshold is relatively low, in addition to the traditional automotive chipset vendors such as NXP, Renesas, Infineon, and many other chip companies and start-ups to enter this market, many participants, but the market research organization Market Beat pointed out that the current market is still dominated by the pioneers. Beat pointed out that the current market share is still dominated by the pioneer Mobileye 70% market share of the exclusive position, was established 20 years ago, 13 automobile manufacturers have adopted the company's ADAS solutions, about 135 million vehicles installed its EyeQ series processor, but it is the main promotion of the hardware and software of the closed solution is difficult to achieve differentiation, and the product computing power is still weak, as listed in Table 2, therefore, the main focus is to promote the software and hardware of the closed solution is very difficult to achieve differentiation, and product computing power is still weak, as listed in Table 2, therefore, it is the main focus of the market. However, its main software and hardware closed solution is difficult to achieve differentiation, and the computing power of its products is still weak, as listed in Table 2, so it is no longer favored by car manufacturers and has switched to cooperate with latecomers such as Nvidia, Qualcomm, and Horizon.

表2、自動駕駛用處理器之主力產品的運算能力比較

資料來源 : 各公司;智璞產業趨勢研究所整理,2024/02

附帶一提,由於運作環境具有振動量大、粉塵多、電磁干擾強、溫度變化劇烈等特點,所以車用晶片對於耐候度、可靠性和使用壽命要求更高,必須通過可靠度標準AEC-Q100、品質管制標準ISO/TS16949、功能安全標準ISO26262等認證,說明如下 :

- AEC-Q100是針對車用晶片失效機制的測試標準,從設計、製造、封裝、電性測試、可靠度試驗等階段都有嚴謹的驗證項目,分成Accelerated Environment Stress、Accelerate Lifetime Simulation、Packaging/Assembly、Die Fabrication、Electrical Verification、Defect Screening、Cavity Package Integrity等7大類。

- ISO/TS16949是由國際汽車推動小組(IATF)制定專用於汽車及其零組件廠商的品質標準,它是在ISO9000的基礎上融合美國QS9000、德國1、義大利AVSQ及法國EAQF等先進國家的汽車業品質管理系統,其適用範圍包括:(1).部件或材料;(2).熱處理、噴漆、電鍍或其它最終加工服務;(3).其它顧客規定產品。其證書效期三年,效期內每年至少檢查一次,可以由IATF認證的稽核員或認可的認證單位進行,三年期滿後需要重新認證。

- ISO26262是由是國際標準化組織(ISO)與國際電工委員會(IEC)合作針對裝設在量產道路車輛的電子電氣系統訂出之安全規範,適用於駕駛輔助、動力和車輛動態控制系統,從管理、開發、生產、經營、服務維修至報廢回收都有規定應執行的方法與步驟。它採用車輛安全程度等級(ASIL)來評斷系統需符合之功能安全程度,等級越高的系統功能安全要求及目標就越嚴謹。

全球自動駕駛晶片技術發展概況剖析

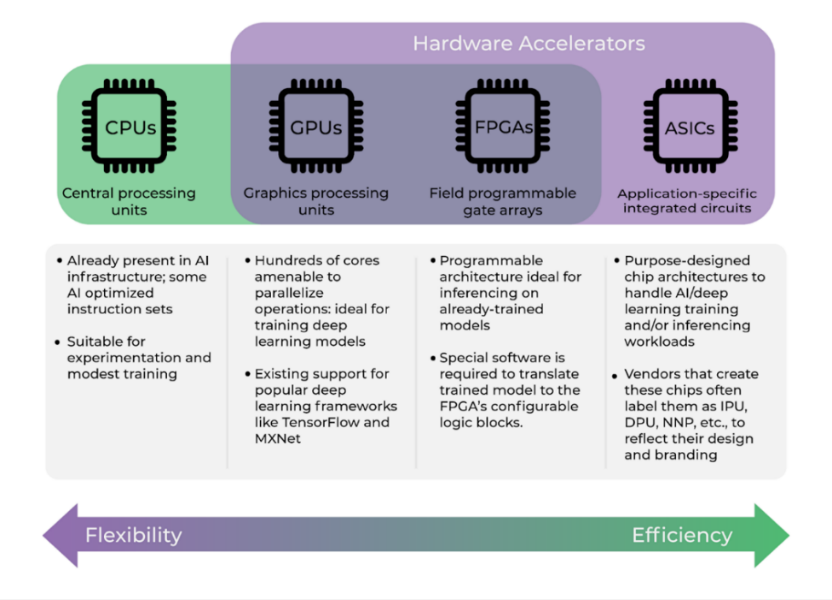

傳統汽車通常採用MCU為控制晶片,隨著電子電氣架構朝向集中式發展,各功能的ECU會將收集資訊傳遞至MCU進行處理和運算,故功能越複雜的車款對MCU性能要求也越高,使其產品已由8位元發展至32位元以滿足高效運算需求。然而到了自動駕駛時代對處理器的運算能力要求暴增,MCU沒法滿足其需求,導入AI已成必然趨勢。當前自動駕駛用處理器晶片使用中央處理器(CPU)搭配AI加速器的系統單晶片(SOC)架構,前者用用定位、決策等邏輯運算,後者用於目標識別、追蹤等任務。AI加速器現有圖形處理器(GPU)、特殊應用積體電路(ASIC)、現場可程式化邏輯閘陣列(FPGA)等類型,其AI應用特性如圖3所示。

圖3、CPU、GPU、FPGA、ASIC在AI應用特性

資料來源 : GSA Global

當前自動駕駛用SoC架構多為CPU搭配GPU或ASIC。因為開發機器視覺、自然語言處理、感測器融合、目標識別等與自動駕駛有關技術所採用的深度學習訓練多以GPU為硬體加速器,故為主要採用的AI加速器類型,不過其缺點是功耗大,所以部分廠商改用採針對特定功能優化設計的ASIC,如張量處理器(TPU)、資料處理器(DPU)和神經網絡處理器(NPU),其優勢是處理速度更快且功耗更低。Nvidia、Tesla的處理器架構是CPU+ GPU+ASIC,Mobileye和地平線則是CPU+ ASIC。在FPGA部分,指標大廠Xilinx以車規級Zynq UltraScale+ MPSoC晶片與Continental、百度等廠商合作開發自動駕駛應用。

February_Self-driving ICs|Analysis of Global Self-driving IC Market Development (Part1)

February_Self-driving ICs|Analysis of Global Self-driving IC Market Development (Part1) February_Self-driving ICs|Analysis of Global Self-driving IC Market Development (Part3)

February_Self-driving ICs|Analysis of Global Self-driving IC Market Development (Part3)