Corporate News|FSMC 2026 Q1 Press Conference

TSMC 2026 First Quarter Facts and Figures

Author: Mr. Lin Wei Zhi, Executive Vice President, Ji-Pu Industrial Trend Research Institute

TSMC held its first quarter 2026 press conference yesterday (16th). TSMC's Q1 2026 results benefited from strong demand for advanced process technologies, with revenues of $1.134 trillion, up 35% year-on-year, higher than the estimated $1.12 trillion. In the second quarter, strong demand for advanced process technologies will continue to support performance, with revenue expected to be in the range of $39 billion to $40.2 billion.

Highlights of TSMC's First Quarterly Financial Results

- Single-quarter revenue of ~NT$1,134.1B, QoQ +8.4%, YoY +35.1%

- Gross profit margin 66.21 TP3T, QoQ +3.9, YoY +7.4

- Operating margin of interest 58.11 TP3T, QoQ +4.1, YoY +9.6

- After-tax net income of approximately NT$572.48 billion, QoQ +13.2%, YoY +58.3%

- EPS (Earnings Per Share) : NT$22.08, QoQ +13.2%, YoY +58.3%

TSMC's Q1 2026 revenue was NT$1.134T, up 35% YoY, and after-tax net income reached NT$572.48B, up 58.% YoY, beating the previous estimate of NT$542.4B by about 6%. Operating income also exceeded the estimate of NT$623.8B, reaching NT$659.0B.

Gross margin was the outstanding highlight of the quarter. TSMC's gross profit rose to 66.2%, an increase of nearly 4 percentage points from 62.3% in the previous quarter, and significantly exceeded the market forecast of 64.5%.

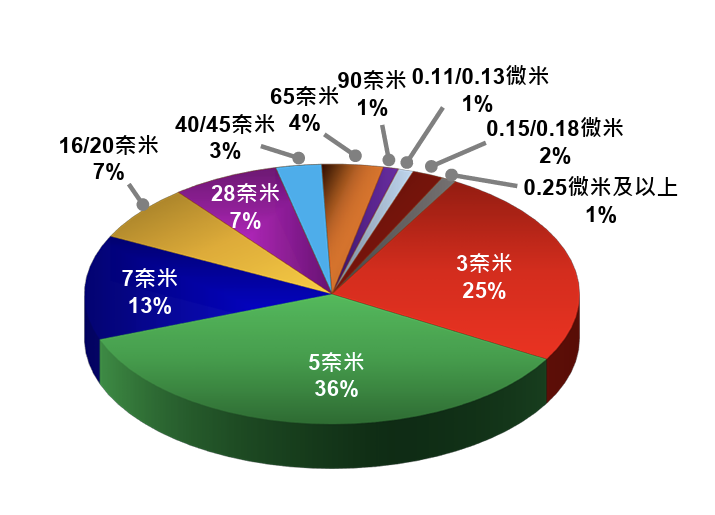

Q1 2026 Process Revenue Share

Shipments of 3nm process accounted for 25%, 5nm process accounted for 36%, 7nm process accounted for 13%, and advanced process (7nm and above) accounted for 74% of the overall sales.

TSMC 2026 Q1 Revenue Share

Source : TSMC

Q2 single-quarter revenue up to $40.2 billion

Looking ahead to the second quarter, benefiting from the strong demand for advanced processes such as AI and high-performance computing, single-quarter revenue is estimated to reach $39 billion to $40.2 billion, a quarterly increase of approximately 10%, and an annual increase of 32%, which is better than the market's expectations, and the AI-driven semiconductor landscape is still in an uptrend cycle. TSMC emphasized that second-quarter revenue growth was mainly driven by advanced processes, especially 3-nanometer and 5-nanometer demand, and the continued expansion of HPC platforms driven by AI servers and data center applications. In the first quarter, HPC accounted for 61% of revenue, the most important growth engine, and this trend is expected to continue in the second quarter.

Capital expenditures of $52 billion to $56 billion unchanged in 2026

TSMC's capital expenditures in 2026 are estimated to be in the range of $52 billion to $56 billion, reflecting demand for AI, 5G and HPC. The company's continued investment efforts demonstrate its optimism about medium- to long-term industry trends.

TSMC's first-quarter capex size of $11.1 billion was 3.51 TP3T less than the $11.51 billion in Q4 2025 and 10.31 TP3T more than the $10.06 billion in capex in the same period last year.

A14 Technology Revealed

Both the 2nm process and the A14 process are on schedule, with the A14 being a leap forward from the N2 by adopting a second-generation nano chip architecture. the A14 can increase performance by approximately 10% to 15% at the same power consumption, or reduce power consumption by 25-30% at the same power consumption, and bring about an increase in wafer density of more than 20%.

TSMC's Chairman, Mr. Chieh-Chia Wei, said that the high level of interest in the A14 from smartphone and HPC customers shows that the demand for advanced manufacturing processes is not a short-term cycle, but a long-term trend. He also emphasized that TSMC maintains a high level of confidence in the "multi-year growth momentum" brought about by AI.

Will the situation in the Middle East impact operations?

Regarding the geopolitical risks in the Middle East, TSMC said that although the recent situation in the Middle East has affected the global energy supply, with the support of the diversified supply chain and governmental cooperation mechanism, it will not cause any substantial impact on production and operation in the short term. TSMC also indicated that it has established a comprehensive enterprise risk management mechanism, adopting a "multi-source supply strategy" for raw materials such as specialty chemicals and critical gases, and maintaining a safe inventory level to minimize the impact of unforeseen events.

Ji-Pu's point of view.

1. 2026 revenue and earnings growth trajectory remains in line with our expectations at this time.

2. The tone of the entire presentation conveyed a clear message: TSMC believes that the investment cycle for AI infrastructure is not yet over, and that 2026 is not a capex year. Management's upward revision of full-year capex guidance to the upper end of the $52-$56 billion range supports this judgment.

3. N3 is currently the tightest process capacity. In terms of TSMC's announced route in the past, N3 was originally a long node, but now it seems that the explosion of AI demand is expected to further extend its life. In response to analyst BofA's question: "The N3 is not a new node, so why is it still expanding production? The answer lies in the fact that most HPCs are currently using N3 production capacity, so the company continues to increase global N3 production capacity (Tainan's new N3 fab is expected to be in the first half of 2027, AZ Fab 2 N3 is expected to be in the second half of 2027, and Japan's JASM Fab 2 is also planning to introduce N3 in the timeframe of 2028), which, in light of the market's application demand and layout, means that N3P's production capacity scale, process performance, and pricing strategy will be the key to the future. Based on the application demand and layout of this market, I think it means that N3P's capacity scale, process performance, and pricing strategy will be the key pass for TSMC to maintain its leading edge in the advanced process area for 3 to 5 years.

4. A market consensus has gradually emerged that foundry is transforming from a traditional manufacturing industry to a high-margin, irreplaceable AI infrastructure. Based on this, TSMC's long-term gross margin framework has been generally upgraded, and 60-62% seems to be the new baseline for the market. However, when N2 enters the volume release stage in the second half of the year, yield creep and depreciation pressure may cause a short-term erosion of gross margins by 2~3%, and the market's tolerance for TSMC may then be in a state of flux, which is worthy of continuous tracking.

5. Analysts from Morgan focused on the competitive landscape of advanced packaging - will solutions such as Intel EMIB create a substantial diversion to CoWoS? CC's response was clear and confident: TSMC still offers the largest package size in the market, CoWoS is the mainstay at this stage, and CoPoS is also under active development. At the same time, TSMC frankly admits the existence of engineering difficulties such as warpage and mechanical stress, and clearly points out that this is exactly where TSMC's core competitive advantage lies. Instead of avoiding the competitive issues, TSMC proactively defined the market trend - the evolution towards large-size packaging - and pointed out that the real moat lies in the system-level engineering integration capability and large-scale mass production execution, which are the highest thresholds and most difficult to replicate. These two points are precisely the highest threshold and the most difficult to replicate.

Corporate News|FSMC 2025 Q4 Press Conference

Corporate News|FSMC 2025 Q4 Press Conference