April_Equipment|Taiwan Semiconductor Equipment Growth Strategy

Taiwan Semiconductor Equipment Growth Strategy

Over the past few years, the semiconductor industry has largely been in a boom phase as global demand for semiconductors has continued to increase due to epidemics, geopolitics and other issues, while driving the expansion of the semiconductor equipment market. According to SEMI's report, global sales of semiconductor manufacturing equipment will total $106.3 billion in 2023, a decrease of 1.3% from $107.6 billion in 2022, but sales of semiconductor manufacturing equipment are expected to rebound in 2024 and hit a new high of $124 billion in 2025, driven by both front-end and back-end manufacturing processes.

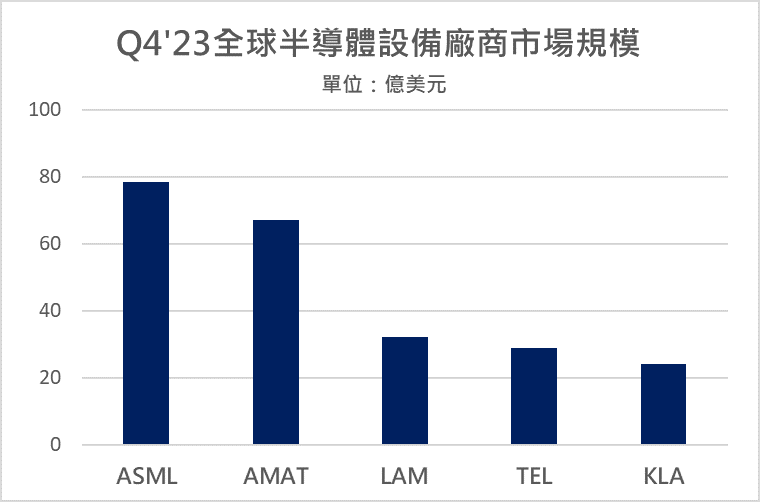

Figure 1: Q4'23 Global Semiconductor Equipment Vendor Market Size

Source: Collated by Ji-Pu Industrial Trend Research Institute 04/2024

- ASML - Netherlands

As the world's No. 1 lithography equipment provider, the company offers EUV and other lithography systems and is the only EUV lithography equipment provider that can offer advanced processes up to 7nm. Its DUV technology is also the mainstay of the semiconductor industry for mass production of wafers, providing immersion and dry micrographic solutions to help wafer makers produce a wide range of nodes and technology processes.

- Applied Materials (AMAT) - USA

The world's largest semiconductor equipment manufacturer, known as the "Semiconductor Equipment Superstore," has a semiconductor business that spans almost the entire semiconductor process, with products that include thin-film deposition (CVD, PVD, etc.), ion implantation, etching, rapid heat treatment, chemical mechanical planarization (CMP), and measurement and inspection equipment. Among them, the ALD system deposits various oxides, metal nitrides, and metals on wafers in a manner that produces a small portion of a single layer at a time, in order to produce the thinnest and most uniform film, which is the key driver of today's flat panel devices and industry transformation.

- Lam Research - USA

Headquartered in Fremont, California, U.S.A., the company has mastered many key technologies for high-tech semiconductor equipment, mainly etching equipment for semiconductor manufacturing, thin film deposition equipment, and cleaning equipment.

- Tokyo Elektronics (TEL) - Japan

Japan's largest semiconductor equipment manufacturer, with products including coating equipment, thermal processing equipment, etching equipment, chemical vapor deposition equipment, cleaning equipment, and testing equipment.

- KLA - USA

A leading manufacturer of semiconductor process inspection and measurement equipment, including defect detection, film thickness measurement, CD measurement and other inspection and measurement equipment.

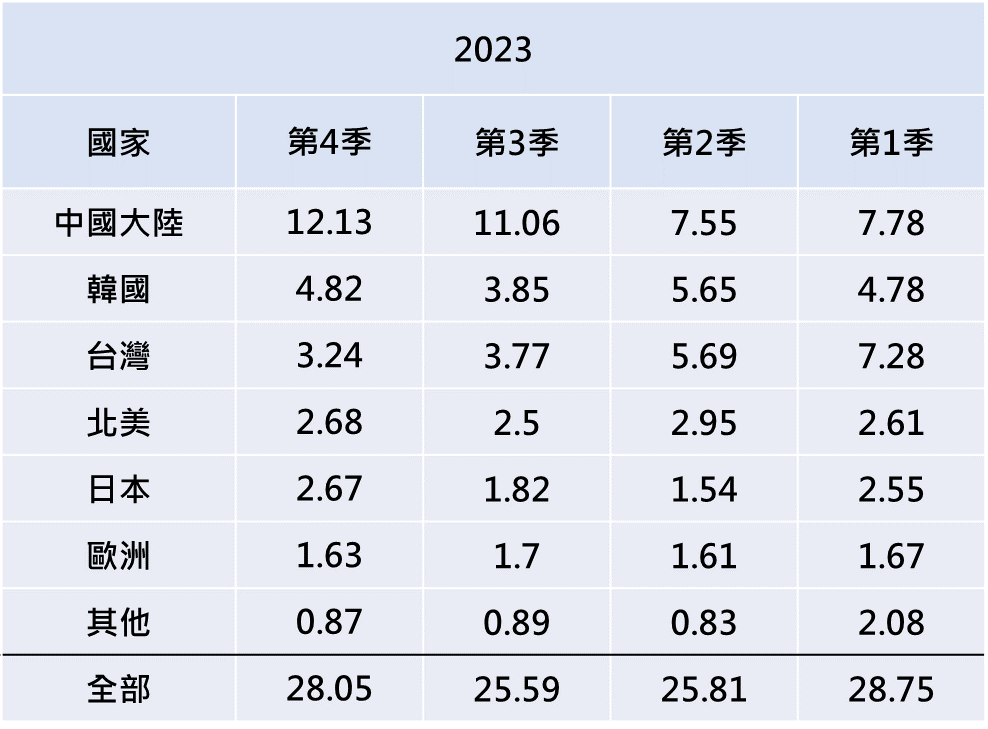

In terms of region, among the top five semiconductor equipment vendors, China is the major market. Except for ASML due to Taiwan TSMC's demand for EUV, the other four vendors derive the largest portion of their revenue from China. Although the impact of inventory depletion and weak wafer demand in 2023 has led to a decline in equipment shipments from Q2 2023 onwards, as shown in Table 1, the shipments from Q4 2023 onwards are expected to be lower. However, the market has rebounded since Q4 2023 and is expected to pick up in the following quarters. According to the report released by SEMI, despite the U.S. export control on advanced process equipment, China's demand for equipment is still at the top of the list, and it is speculated that the company is striving to break through the blockade on advanced processes and showing strong demand on mature processes.

Table 1: Quarterly Equipment Shipments by Region (in billions of dollars)

Source: Organized by Jipu Industrial Trend Research Institute.

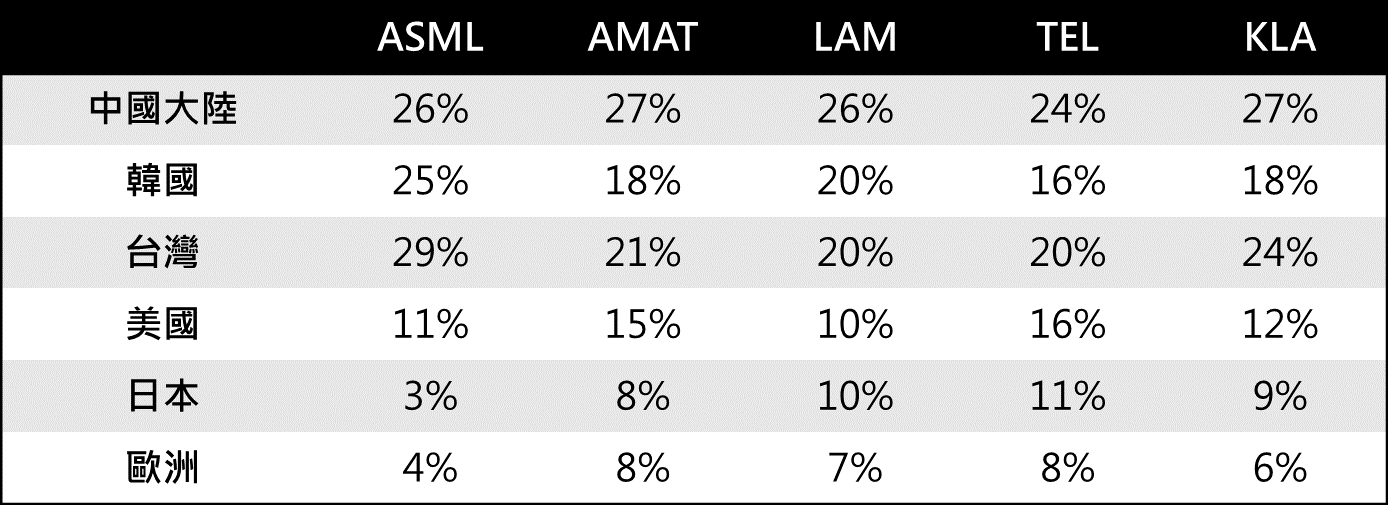

According to ITRI's report, more than 70% of the world's sub-10nm wafers come from Taiwan, so Taiwan has a good share of the revenue of the five largest semiconductor equipment vendors. In ASML's 2023 annual report, Taiwan accounted for the largest share of sales; in the part of AMAT, it accounted for the second largest share of sales. According to the reports released by the companies, in 2023, four companies had the second largest share of Taiwan and one had the first, as shown in Table II. This again reinforces the impression that Taiwan is a globally recognized semiconductor manufacturing center with a strong semiconductor cluster and ecosystem. However, from a different perspective, despite Taiwan's strong technology and ecosystem, China, driven by the end market, is still the main equipment market.

Table 2: Revenue Share of Global Top 5 Equipment Suppliers by Customer Country in 2023

Source: Ji-Pu Industrial Trend Research Institute; Collated by 3/2024

Note: The month of receipt of the accounting year varies from company to company, ASML (January to December), AMAT (November to October), LAM (July to June), TEL (April to March), KLA (July to June).

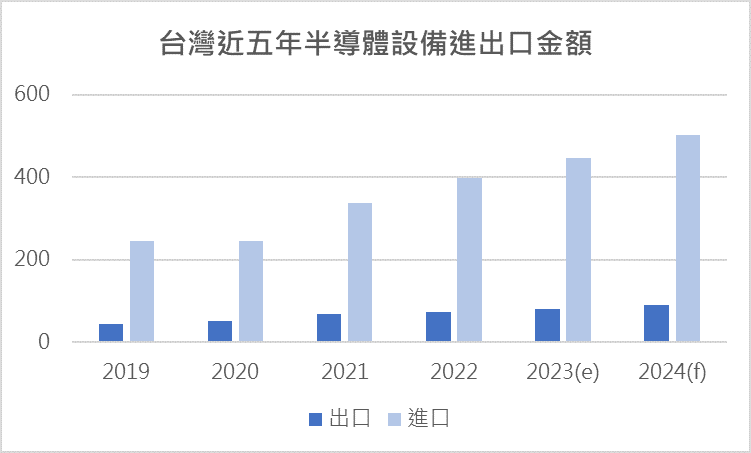

In recent years, Taiwan's direct exports of semiconductor equipment have jumped rapidly, with Mainland China, Singapore, the United States and the Netherlands as the main exporting countries, with the top four countries accounting for more than 70% of total exports. However, Taiwan is one of the world's most important wafer production bases, with a high demand for equipment, even attracting many international semiconductor equipment manufacturers to set up factories in Taiwan. According to ITRI's report, even though the amount of local semiconductor equipment exports has been increasing year by year, the overall export/import ratio is still about 1:5, as shown in Figure 2. Compared to Taiwan's semiconductor manufacturing industry, which stands at the top of the world, semiconductor equipment is still in the development stage and needs more opportunities and growth strategies. The Netherlands is the largest importer, followed by Japan, the U.S., and Singapore. Taiwan's exports of semiconductor equipment to Singapore and Malaysia have increased significantly in recent years, mainly due to the development of the testing and packaging industry in the region, as well as the expansion of investment in production lines in Singapore and Malaysia by major international companies.

Figure 2: Import and Export Value of Semiconductor Equipment in the Past Five Years

Source: Industrial Technology Research Institute (ITRI); Estimated/Organized by Ji-Pu Industrial Trend Research Institute (JPTRI), 04/2024

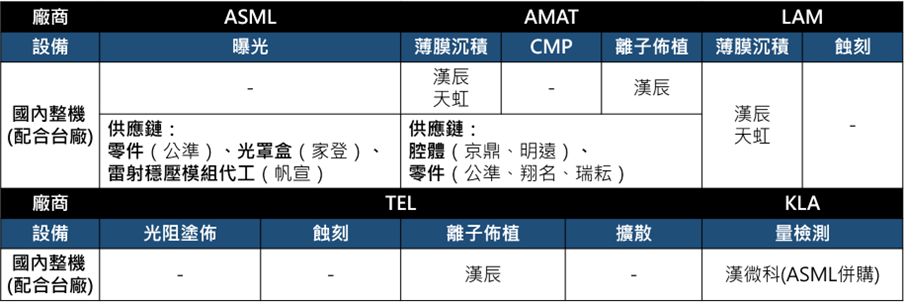

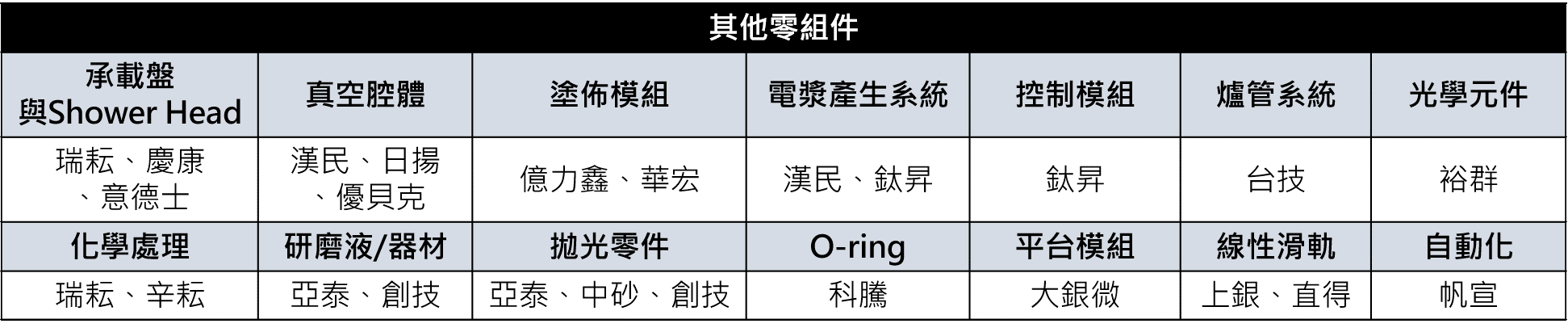

Taiwan's equipment manufacturers mainly focus on traditional packaging equipment, OEM modules and components from major international manufacturers, while advanced process equipment is mainly imported from leading international equipment manufacturers. According to the Customs import and export data, Taiwan's self-sufficiency rate for back-end equipment is about 15%, and the government's goal is to increase it to 40% by 2030. front-end equipment is almost monopolized by large companies, coupled with the fact that front-end equipment takes a longer time to develop and validate, and that Taiwan is a latecomer, it's not easy for Taiwan to join the competition.At present, apart from OEM modules, most of the products are supplied as spare parts.Therefore, the government is promoting the nationalization of semiconductor equipment in the direction of advanced packaging equipment, inspection and measurement equipment and components as a priority. Even so, Taiwan manufacturers still have a good performance. Domestic manufacturers such as Jing Ding, Ruikeng, and Mingyuan in the supply chain of AMAT, as shown in Table 3; Jaden and Fanshun in the supply chain of ASML; and Tiensheng, Hanmin, and Chi-Sheng and other domestic component factories are all Taiwanese suppliers that are in line with the international equipment vendors, as shown in Table 4.

Table 3: Wafer Fabrication Equipment Suppliers in Taiwan

Source: Organized by Jipu Industrial Trend Research Institute.

Note: The - symbol indicates that only components are manufactured in Taiwan.

Table 4: Other Component Manufacturers in Taiwan

Source: Organized by Jipu Industrial Trend Research Institute.

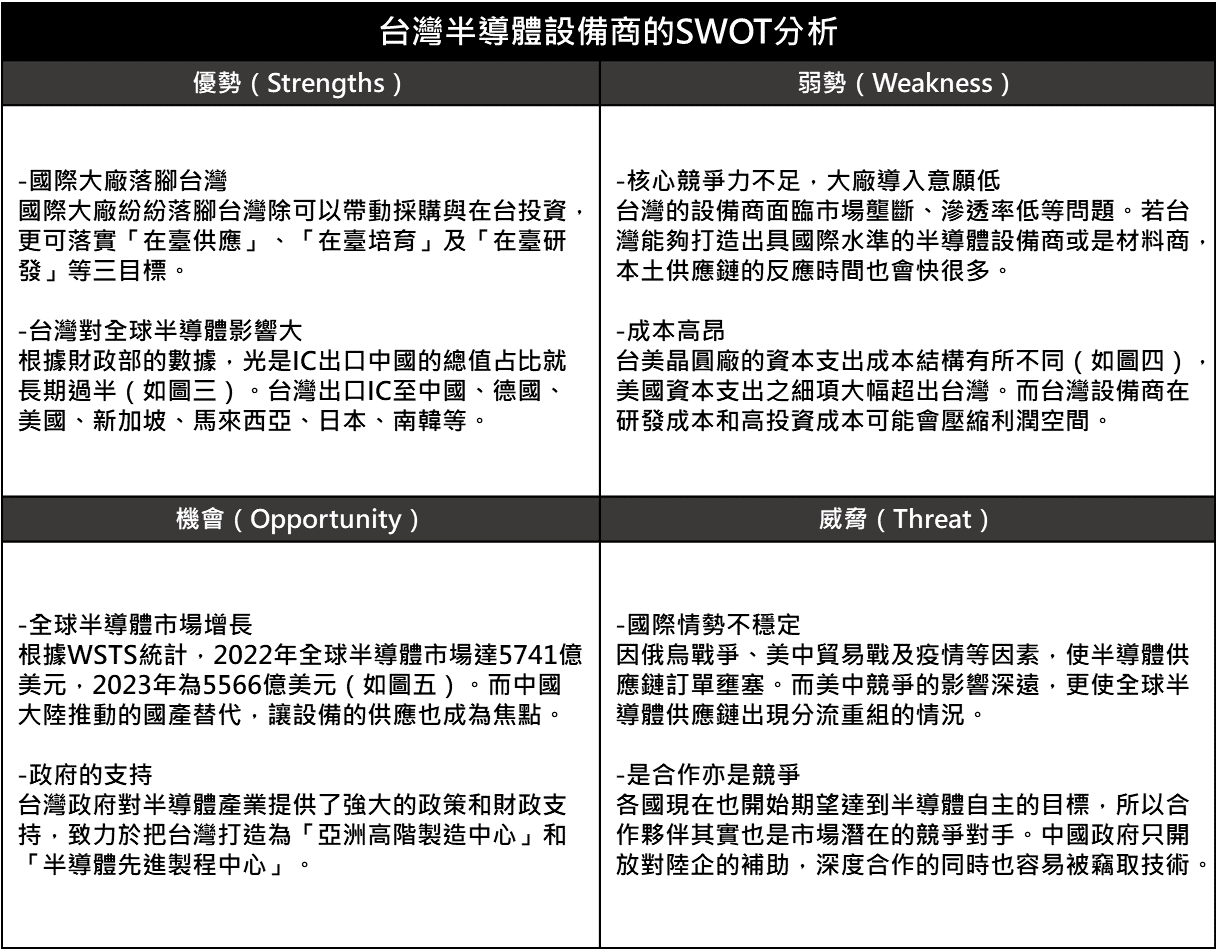

Looking back at history, Taiwan's semiconductor industry has been able to occupy a very important position in the world. In addition to government support, the threats generated by the great power game and the opportunities brought by international trends are not to be ignored; in addition, Taiwan's complete ecosystem and supply chain based on its own strengths have raised the entry threshold for other countries. Although the semiconductor equipment market has been monopolized by large international companies, but in the international situation is also unstable, geopolitical rise in the situation of confrontation, many international semiconductor equipment vendors in Taiwan to set up high-end research and development centers, the role of Taiwan's equipment vendors can be focused on the supply of key components, and with the support of the Taiwan government, Taiwan's semiconductor equipment vendors have the opportunity to penetrate the international supply chain, and to secure a place.

Table 5: SWOT Analysis of Taiwan Semiconductor Equipment Vendors

Source: Organized by Jipu Industrial Trend Research Institute.

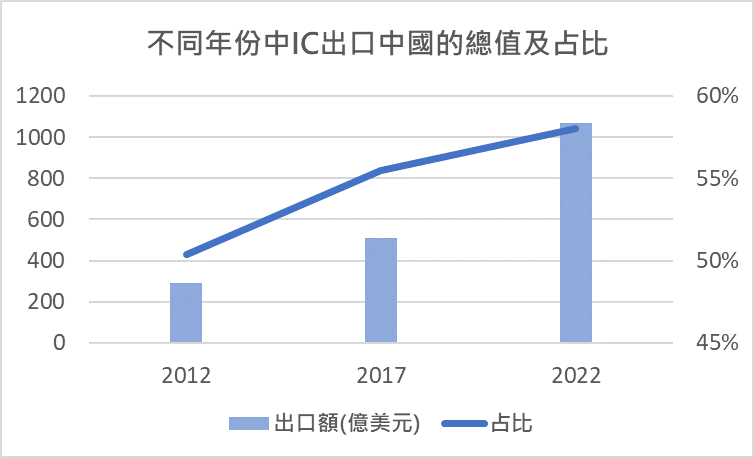

Summarizing the SWOT analysis, we can find that before the Russia-Ukraine war broke out, the international community had already experienced order congestion and even supply chain disruption in the semiconductor supply chain due to the U.S.-China trade war that has lasted for several years, as well as the epidemic and other factors. The far-reaching impact of the U.S.-China rivalry has caused the global semiconductor supply chain to diverge and reorganize, and has gradually created a world where two systems diverge. Taiwan, in the context of the great power game, needs to be vigilant against international competition for our advantageous position, and whether there are attempts to marginalize our country, such as the U.S. to subsidies and customer demand and other means to require TSMC to move the most advanced semiconductor manufacturing to the U.S.; the British government in the G7 summit released a semiconductor strategy, explicitly listed in the U.K. need to reduce the geopolitical sensitivity of the geo-political regions such as Taiwan to reduce the reliance on semiconductor imports. In addition, the Chinese government, in order to strengthen its own semiconductor industry, continued to open up subsidies to mainland enterprises, but also in the past few decades of experience in the experience of fraud gradually smart and efforts to allow the state-supported enterprises to have their own manufacturing technology. Therefore, it is easy to steal technology while cooperating with China.

Chart 3: Total Value and Percentage of IC Exports to China by Years

Source: Ji-Pu Industrial Trend Research Institute

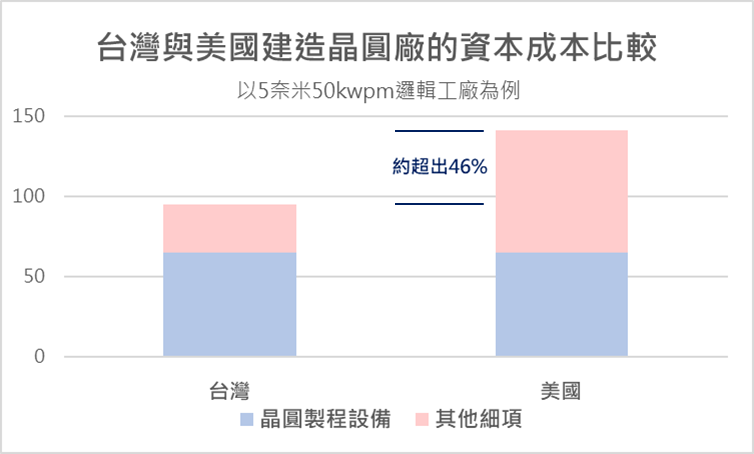

Figure 4: Capital Costs of Wafer Fabs in Taiwan and the U.S.

Source: Ji-Pu Industrial Trend Research Institute

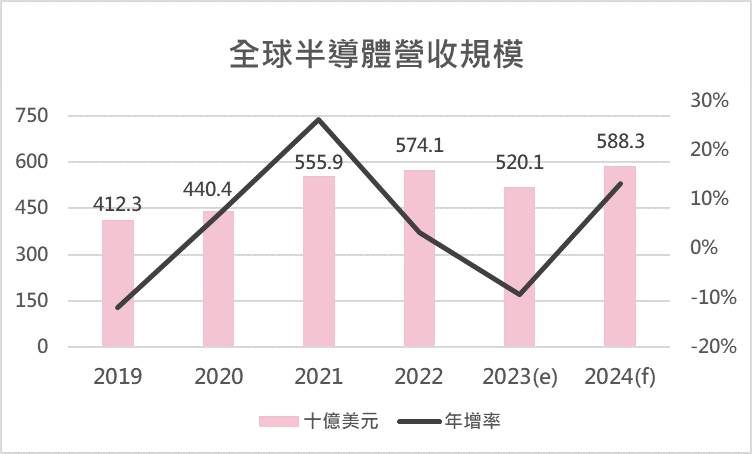

Figure 5: Global Semiconductor Market Size

Source: WSTS; Collated by Ji-Pu Industrial Trend Research Institute

Facing the development of the global semiconductor industry, Taiwan's semiconductor equipment manufacturers have a unique background and strategic positioning, and need to be more flexible means to meet the challenges, making good use of government policies and market trends, there is a very good chance to enhance the status in the world, and increase the proportion of nationalization of semiconductor equipment. Then President Tsai Ing-wen pointed out in 2022 that the semiconductor industry is a very important project for the national policy. Currently, Taiwan's semiconductor equipment mostly relies on imports, and it is strongly expected that the equipment used by the semiconductor industry can reach a certain percentage of nationalization. Looking at Taiwan's semiconductor equipment manufacturers, in fact, there is no lack of bright performance, but the overall market penetration rate is low and most of the supply of parts-based, so it is more difficult to expand profits in the oligopolistic competition in the market, coupled with customer diversity is not high, so it brings the risk of high, high variability and other challenges, so that the local semiconductor equipment vendors are prone to disadvantage in the international arena.

However, in addition to government support, the competitiveness of semiconductor equipment depends on the accumulation of basic science and the long-term investment of R&D resources. Because of Taiwan's past focus on the semiconductor industry, the latter two points are relatively weak. Therefore, how to grasp the international trend, eliminate threats and create opportunities will be an important issue for Taiwan's semiconductor equipment companies to face. From the above analysis, it seems that in the unstable global situation, Taiwan semiconductor equipment companies need to be able to adjust their strategies more flexibly, strengthen the flexibility and risk resistance of the supply chain, pursue a balance between cooperation and competition, and at the same time, respond to the government's policies and subsidies, and make good use of the resources provided by the government in order to enhance competitiveness in order to be able to achieve sustainable development. Against this background, we believe that Taiwan's semiconductor equipment vendors can try to "base on the mainland, aiming at Europe and the United States" strategic approach, boldly enter the mainland market, using the demand for domestic substitution in China as a test field, as a means of entering the supply chain of major international companies. Considering the urgent need for semiconductor equipment in China and the political and trade tensions, it is difficult to import from international manufacturers, Taiwan's semiconductor equipment manufacturers should pay more attention to understanding and meeting the needs of the mainland and the market dynamics, the vast market as a stage to demonstrate their core competencies in technology, although they may face some copying, imitation of the threat, but this highlights the importance of sustained innovation and technological advances. Although we may face some threats of copying and imitation, this emphasizes the importance of continuous innovation and technological progress. At the same time, we also actively seek opportunities to cooperate with major international companies in Europe and the United States, with the goal of entering their supply chain, OEM key modules and components, to capitalize on Taiwan's strengths, and to form a closer cooperative relationship. While ensuring technology leadership, we are actively seeking to expand and diversify domestic and international markets, and are working closely with the government and upstream and downstream of the industry chain to jointly promote Taiwan's semiconductor industry and move toward higher goals.

March_Smart Capsule Chipset Topics|Global Smart Capsule SoC Chipset Supplier Product Technology Analysis(Part2)

March_Smart Capsule Chipset Topics|Global Smart Capsule SoC Chipset Supplier Product Technology Analysis(Part2) May_Semiconductor Technology|Trends in Semiconductor Process Technology from TSMC Technology Forum

May_Semiconductor Technology|Trends in Semiconductor Process Technology from TSMC Technology Forum